Back to Top

.avif)

Asia

Rates

- Carriers began a price war for the first half of October in order to fill additional loader vessels out of China.

- Approximately 20,000 TEU of capacity was added to the market by Yang Ming, OOCL, Hapag Lloyd, TS Lines, SeaLead, and Cosco. This has resulted in spot rates of USD3400-4000 per FEU, dependent on service.

- While the market looks soft, carriers remain optimistic that demand will increase in the second half of the month. GRIs have started to filter through. My gut feeling is that we may see an initial surge as factories reopen after the holiday; however, it will be short-lived.

- Gold Star Line is implementing a GRI of USD500/TEU, effective 15th October. This will impact all cargo ex NEA to AU.

- There is the threat of PSS (Peak Season Surcharge) on the 1st November.

- South East Asia remains congested in most key hubs, with rates sitting at USD4800-5000 per FEU.

- Vietnam has limited space - particularly with Maersk, OOCL out of Ho Chi Minh. ANL also reports equipment shortages.

- Space ex Malaysia is selling out fast, with many carriers increasing rates in the second half of the month.

- Typhoon Bebinca, the strongest Typhoon to hit China in 75 years, hit Shanghai mid-September. The Typhoon weakened as it moved inland, however the severity has impacted vessel schedules and the knock on effect will be realised for the next couple of weeks. Source: https://www.abc.net.au/news/2024-09-17/typhoon-bebinca-hits-china-shanghai/104358550

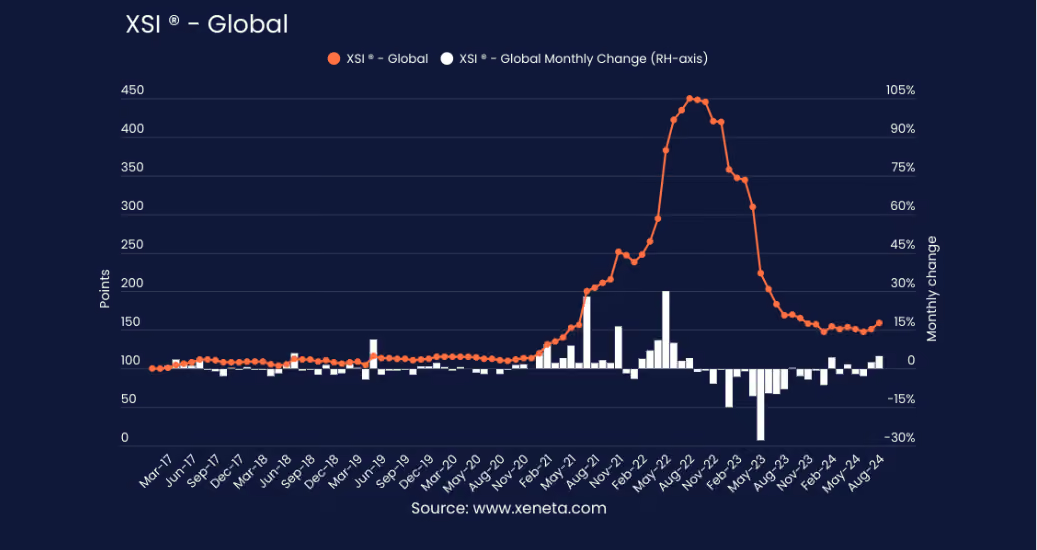

- The gap between long-term contract pricing and the spot marked is narrowing. The Global XSI (Xeneta Shipping Index) increased by 5% in August, twice the rate of July. Source: Xeneta

Capacity

- Extra loader capacity has resulted in an additional 20,000 TEU in the China market. Space is plentiful at present, but may start to tighten after Golden Week.

- There are ample sailings for the first half of October, with a single blank sailing for the JKN service in week 42.

- EMC/COSCO has a severe shortage of 20'NOR & 40'NOR equipment.

- JKN service has a blank sailing in 2nd. week of Oct.

- A3N service has a blank sailing in 2nd. week of Oct.

- CAT service has a blank sailing in 1st. week of Oct.

- CA2 service has a blank sailing in 3rd. week of Oct.

Schedule Reliability

- In August 2024, global schedule reliability improved by 0.7 percentage points M/M to 52.8%. Schedule reliability in 2024 has stabilised within the 50%-55% range. While disappointingly low, the minimal volatility this year does give shippers a relatively good idea of what to expect M/M. On a Y/Y level, schedule reliability in August 2024 was -10.2 percentage points lower. The average delay for LATE vessel arrivals increased by 0.03 days M/M to 5.28 days, which is only surpassed by the pandemic highs of 2021-2022. On a Y/Y level, the August 2024 figure was 0.62 days higher. Maersk was the most reliable top-13 carrier in August 2024 with schedule reliability of 54.7%, followed by Hapag-Lloyd with 54.3%. Another 8 carriers were above the 50% mark, with PIL the least reliable at 37.2%. Source: https://www.sea-intelligence.com/press-room/288-global-schedule-reliability-remains-stable-at-50-55-in-2024

North America: US & Canada

- Hurricane Milton reached category 5 status with winds of 165 miles per hour. This has prompted one of the largest evacuations in Florida history - over 5.5 million residents. 17.4% of all gas stations in Florida are now out of fuel and roads are in gridlock as the evacuation continues. Aircraft are grounded and there will be little to no access until the storm passes. Source: https://www.theguardian.com/us-news/2024/oct/08/florida-hurricane-milton-evacuation

- MSC announces an Emergency Operation Surcharge (EOS) implementation, applicable to all shipments directed to U.S. Gulf and East Coast Ports. Unless otherwise specified, all charges of reefer and special equipment for open top, flat rack, and tank containers are the same as the below tariff for dry cargo: USD $1500 per 20' container & USD $3000 per 40' container

- The rules surrounding ‘de minimis’ allowances could change if the Biden Administration’s plea to reduce the threshold are passed. While this has predominantly surrounded e-commerce trade, this will put added scrutiny on US imports of smaller packages. Source: https://www.supplychainbrain.com/articles/40409-will-customs-crackdown-on-de-minimis-shipments-slow-cross-border-commerce

- U.S. East Coast and Gulf Coast ports came to a standstill after members of the International Longshoremen’s Association (ILA) began walking off the job after 12:01 a.m. ET on October 1. The ILA is North America’s largest longshoremen’s union, with roughly 50,000 of its 85,000 members striking. The USMX offered a nearly 50% wage hike over six years, but that was rejected by the ILA. The 14 ports impacted are Boston, New York/New Jersey, Philadelphia, Wilmington, North Carolina, Baltimore, Norfolk, Charleston, Savannah, Jacksonville, Tampa, Miami, New Orleans, Mobile, and Houston. Source: https://www.cnbc.com/2024/10/01/east-coast-ports-strike-ila-union-work-stop-billions-in-trade.html

- After 3 days, the US port strikes were suspended. A tentative agreement was reached with the ILA, with negotiations to resume on 15th January 2025. Source: https://abcnews.go.com/US/dockworkers-strike-suspended-sources/story?id=114445386

- Although the port strike was shortlived, a backlog still remains. More than 40 ships were waiting to dock, and while operations ceased for only 3 days, there is now a large volume of containers to unload. Source: https://container-news.com/usec-port-strike-ends-but-supply-chains-will-take-weeks-to-recover/

- With disruptions hitting US ports, a spike in airfreight demand is already commencing. With airfreight capacity significantly more limited than the container trade, demand will exceed supply. The airlines will take advantage of a hot market and we can expect the pricing to reflect this. Source: The Loadstar

- Dockworkers kicked off a three-day strike at the Port of Montreal on Monday, shutting down two terminals that handle more than 40 per cent of the container traffic at Canada's second-largest port. Some 350 longshore workers walked off the job at the Viau and Maisonneuve Termont terminals at 7 a.m. Monday, part of a limited strike amid contract talks. The strike is expected to last until Thursday morning. Source: CBC

Europe

- Dockers in Germany’s North Sea ports have approved a proposed new collective agreement in a vote by members of the Verdi union. A majority of 77.6% of the approximately 11,500 members working in the North Sea ports voted in favor of the agreement, which comes into force after being approved by the union’s national tariff commission. The new collective agreement is valid until the end of July next year. Source: https://shippingwatch.com/Ports/article17495566.ece

- From the 31st of October 2024 an Entry Summary Declaration (ENS) is mandatory for all shipments destined for or transiting the 27 European Union countries, and three other countries: Northern Ireland, Norway and Switzerland. This regulation applies also to freight remaining on board. This is part of the upcoming third release to European Union’s Import Control System 2 (ICS2). For more information: https://taxation-customs.ec.europa.eu/customs-4/customs-security/import-control-system-2-ics2-0/import-control-system-2-release-3_en

- Port congestion in Europe has severely vessel berthing. Delays of up to 30 days has been reported in some ports.

Global Air Freight

- Bottlenecks are forming at key South East Asian hubs ahead of peak season. Singapore and Manila are already showing signs of congestion, with the situation in the Philippines critical. Source: https://theloadstar.com/bottlenecks-begin-to-form-in-asia-as-air-peak-season-approaches/

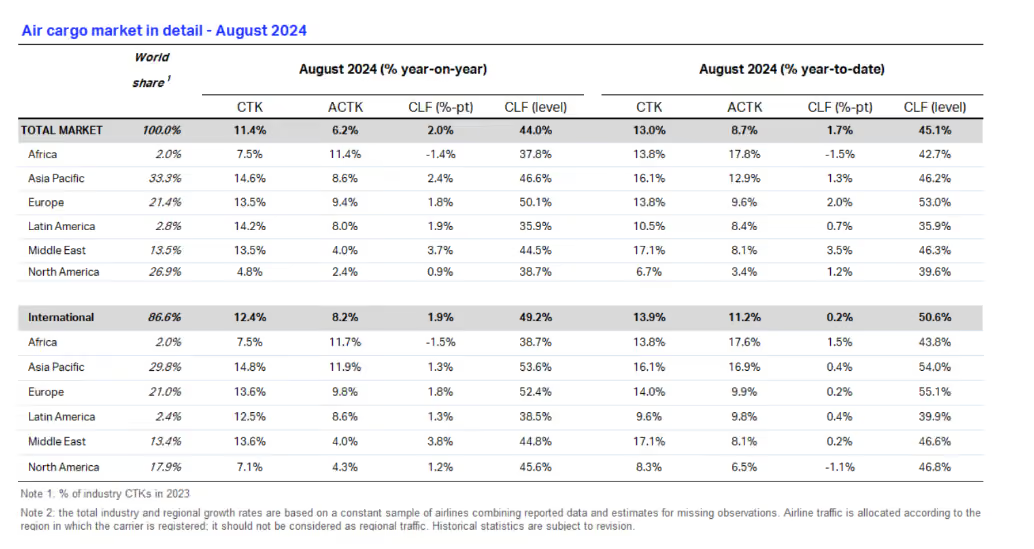

- Global Cargo Tonne-Kilometers (CTK) increased by 11.4% year-on-year (YoY) last month, delivering the ninth consecutive month with double-digit demand growth and the second straight month with record year-to-date demand levels. Net of seasonal adjustment, demand contracted by -0.2% month-on-month (MoM).

- International CTK added 12.4% relative to last year, driven by all regions and major trade lanes. Asia Pacific carriers recorded the largest expansion with 14.8% YoY, and demand on the Middle East-Europe trade lane outpaced all others with an outstanding 28.9% annual surge.

- Global air cargo capacity, measured in Available Cargo Tonne-Kilometers (ACTK), saw 6.2% growth YoY in August, seeing slower growth than in the months prior but at the same time delivering record capacity levels.

- Despite global record capacity and falling fuel prices, the global air cargo yield maintains a moderate upward trend.

- Airlines registered in Asia Pacific saw the highest annual growth in international CTK, registering 14.8% YoY. European and Middle Eastern airlines followed with 13.6%. Souce: IATA

General news

- The Red Sea struggles show no signs of easing. A drone struck a ship in the Red Sea in a suspected attack by Yemen’s Houthi rebels on Tuesday 1st October. The Red Sea has become a battlefield for shippers since the Houthis began their campaign targeting ships traveling through a waterway that once saw $1 trillion a year of cargo pass through it. Houthis have targeted more than 80 merchant vessels with missiles and drones since the war in Gaza started in October. They have seized one vessel and sank two in the campaign that has also killed four sailors. Other missiles and drones have either been intercepted by a U.S.-led coalition in the Red Sea or failed to reach their targets, which have included Western military vessels. Source: https://abcnews.go.com/International/wireStory/suspected-yemen-houthi-rebel-attack-targets-ship-red-114374661

- Gale force winds are impacting Melbourne and Fremantle Ports, forcing vessels to remain anchored at sea, and vessels in port forced to evacuate their berths. The situation in Fremantle has improved, however, Melbourne terminals are experiencing container toppling and depot closures. Source: https://www.thedcn.com.au/region/australia/gales-send-fremantle-vessels-back-to-sea/

- Japanese logistics group Nippon Express Group has acquired all shares in German competitor Simon Hegele, based in Karlsruhe. Simon Hegele employs almost 2,800 people and has a turnover of more than EUR 300m, according to a press release announcing the sale. Source: https://shippingwatch.com/logistics/article17497322.ece

- The looming sale of German forwarder, DB Schenker, to Danish giant, DSV may be stalled with trade union, EVG, voting against the sale. The deal is worth EUR14.3 billion and if successful, DSV would acquire a workforce of approximately 147,000 employees across 90 countries. Source: https://theloadstar.com/union-members-on-db-board-set-to-vote-against-dsv-sale/

Interesting articles

- https://www.explorate.co/resources/the-problem-with-supply-chain-data

- https://primemovermag.com.au/acfs-port-logistics-launches-all-electric-pilot-program/

- https://www.npr.org/2024/09/30/nx-s1-5133462/hurricane-helene-quartz-microchips-solar-panels-spruce-pine

- https://theloadstar.com/indian-government-intervenes-to-help-exporters-facing-higher-costs/

- https://container-news.com/container-shipping-braces-for-rate-collapse/

- https://theloadstar.com/india-takes-rmg-market-share-from-strife-ridden-bangladesh/

- https://www.supplychainbrain.com/articles/40404-why-inventory-management-isnt-just-for-christmas

- https://www.sea-intelligence.com/press-room/289-strike

- https://www.aircargonews.net/business/supply-chains/port-strike-suspension-relieves-air-cargo-pressure-but-peak-outlook-remains-tight/

- https://www.mckinsey.com/industries/travel-logistics-and-infrastructure/our-insights/ready-for-takeoff-the-airline-retailing-opportunity?cid=wkndrd-eml-nsl-mip-mck-ext-----&hlkid=be776a3749194733bc0dd18397270c5b&hctky=15553354&hdpid=43431931-e84e-4daf-811a-774577a52e38

.avif)

Brad Turnbull

Head of Pricing & Procurement

Experienced Business Development Manager with a demonstrated history of working in the logistics and supply chain industry. Skilled in Import/Export, Freight Transportation, Freight, Warehouse Operations, and Overseas Networking.

References

Frequently Asked Questions

Explorate gives supply chain managers one real-time view across ever forwarder, lane and mode without replacing your current process, partners or systems.

What is Explorate and what services does it provide?

How is Explorate different from a traditional freight forwarder?

Why does Explorate provide these Market Updates?

How can I use the data in these updates to optimise my supply chain?

Where does Explorate source the intelligence for these reports?

Can I request my own quote?