.png)

What's happening in global freight

Global shipping is under renewed strain as container freight rates continue to slide for the 13th consecutive week, driven by oversupply and weaker demand. Geopolitical tensions and changing tariff regimes, particularly between the U.S. and China, are adding further volatility to trade flows and routing decisions. At the same time, many companies are racing to strengthen supply chain resilience through technology, embracing AI, analytics, and automation, and shifting toward regional warehousing or nearshoring to minimise disruption risk. Cybersecurity has also emerged as a critical concern, with nearly one-third of supply chain leaders reporting recent cyberattacks on their networks.

Global freight trends

.png)

Top three watch-points in the global supply chain for the coming month:

- Rate stability and capacity management After months of softening, container freight rates may finally hit the floor. Carriers are beginning to announce more blank sailings and vessel re-deployments to stabilise the market. Expect further adjustments through November, especially on Asia–Europe and Trans-Pacific routes as carriers try to restore rate discipline.

- Trade policy and geopolitical pressure Shifts in tariff structures and escalating geopolitical tension are influencing routing, with many shippers re-evaluating sourcing outside of China. Southeast Asia, India, and Mexico continue to benefit from nearshoring and diversification trends, but political uncertainty in several regions could still disrupt the consistency of supply.

- Supply chain resilience and cybersecurity With rising cyber incidents targeting logistics networks, companies are prioritising digital resilience as much as physical. Investments in end-to-end visibility tools, AI-driven forecasting, and secure data sharing are now central to maintaining operational stability.

For Oceania importers, this means cheaper freight in the short term, but with volatility ahead as space tightens into year-end. Many are locking in rates early, diversifying supplier bases, and investing in tech-enabled supply chain tools to stay agile.

In short: Costs are down, risk is up - now’s the time to renegotiate, diversify, and digitise before the next market swing.

Australia

Australia

It’s been a relatively steady week across the major Australian ports, though a few hotspots are worth keeping on your radar.

- Brisbane is still feeling a mild pinch, with average vessel waiting times hovering around the two-day mark. Carriers are juggling berth availability and weather windows, but overall throughput remains consistent.

- Melbourne experienced high winds, closing container parks last week. Delays of up to 3 days can be expected.

- Sydney operations are seeing delays of up to 4 days.

- Flinders (Adelaide) has stayed relatively clear of congestion this week. Infrastructure upgrades at the Outer Harbor terminal continue to progress, positioning the port well for future capacity — but for now, no disruptions to note.

- Fremantle shows light congestion, though nothing outside the norm. Live tracking data suggests vessels are moving steadily through the terminal, with some minor bunching related to weather earlier in the week.

In summary: conditions remain largely favourable for importers and exporters, but as we edge closer to the pre-Christmas surge, keeping an eye on vessel bunching and capacity adjustments will be key. Freight is flowing, for now, but the tide can turn quickly.

North East Asia

North East Asia

The China-Australia trade lane remains busy and resilient. Freight rates have firmed after an extended period of softness, with carriers largely aligned in their mid-October adjustments. MSC has adopted a more aggressive approach to fill recent extra-loader capacity, while premium carriers continue to hold firm, reflecting confidence in the strength of demand.

Ocean freight rates

- Budget Services: Budget carriers are maintaining consistent rate levels across all major ports. Capacity remains healthy, but space is tightening as bookings for the final two weeks of October surge. Shippers relying on this tier should confirm allocations early to avoid rollovers. Rate levels between USD1300 - 1400 per TEU.

- Mid Tier Services: Carriers within this alliance are prioritising consistency over competition, which is helping sustain market confidence during the pre-holiday rush. Rate levels sitting at approximately USD1400 per TEU.

- Premium Services: Premium carriers continue to command the top tier of the market, targeting customers who value reliability and priority uplift. With strong brand loyalty and minimal rate sensitivity, these services are maintaining full vessels without the need for promotional pricing. Rate levels between USD1550 - 1650 per TEU.

Capacity and schedule reliability

Multiple blank sailings and reduced extra loaders are tightening space availability through the second half of October. The pre-holiday cargo surge has overbooked vessels departing between 9–19 October, pushing new bookings toward the end of the month.

On the West Coast, Fremantle and Adelaide remain relatively stable, though congestion in Singapore has created some flow-on delays and higher utilisation across the network.

North East Asia bottom line

- Space is tight, not rates: Despite rate increases, demand remains strong and vessels are sailing full. Expect continued rollovers on East Coast services.

- Market discipline is holding: Carriers are managing capacity through blank sailings rather than rate wars, helping stabilise the lane through late October.

- Peak pressure is building: Pre-holiday demand and ongoing transhipment congestion (particularly via Singapore) may extend lead times into early November.

South East Asia

South East Asia

.avif)

Southeast Asia is once again under weather pressure, with Tropical Storm Matmo marking the fourth typhoon in a month. Heavy rainfall exceeding 250mm is forecast across northern Vietnam, southern China, and the South China Sea, bringing flash flooding, high winds, and challenging sea conditions.

Operational impacts are most visible across Vietnamese ports, where vessel schedules are facing delays of up to several days. Cai Mep and Ho Chi Minh City remain congested as adverse weather slows quay operations and limits barge movements. Inland flooding is disrupting road transport to major manufacturing and export zones, creating flow-on effects at transshipment hubs like Singapore and Port Klang, where arrival bunching and high yard utilisation (85–95%) are adding pressure through mid-October.

Spot rates for the second half of October remain steady, but early indicators suggest a potential rate uptick from November as carriers recover lost productivity and reposition equipment.

Ocean freight rates

Capacity and schedule reliability

South East Asia bottom line

- Operational delays are spreading across key Southeast Asian ports due to ongoing typhoon activity and flooding.

- Vietnamese gateways are the hardest hit, with congestion now extending through regional feeder and transshipment hubs.

- Rates are steady for now, but capacity adjustments and weather-related inefficiencies could lift pricing into November.

North America

North America

The TPEB trade lane is entering a soft patch following the slowdown during Golden Week in Asia. Blank sailings across Weeks 41 and 42 are an intentional capacity control measure, reducing available space to approximately 62–69% of normal operations. Capacity is set to rebound to around 83% in Week 43, but this recovery is likely to create a short-term oversupply as demand remains low to flat.

Freight rates have continued to soften, prompting carriers to announce a General Rate Increase (GRI) effective October 15 in an effort to stabilise pricing. The next Shanghai Containerized Freight Index (SCFI) reading, due October 10, will provide clearer direction on market sentiment. Peak Season Surcharges (PSS) originally planned for mid-October have now been postponed to November 1, reflecting weak near-term demand.

US/Canada bottom line

- Capacity management is key: Carriers are actively blanking sailings to prevent further rate erosion.

- Demand recovery is slow: Despite the return of capacity post–Golden Week, bookings remain soft.

- Rates are under pressure: GRIs may hold briefly, but sustained increases will depend on whether demand strengthens through late October.

Europe

Europe

.png)

The FEWB trade remains flat following the recent Golden Week holidays in China. To mitigate slow demand recovery, liners pre-loaded their roll pools before the break, overbooking by 20–50% to optimise utilisation in case post-holiday volumes failed to rebound, as seen in previous years.

Capacity management continues to be the main lever for stabilisation. The existing blank sailing program will maintain around a 10% capacity reduction in Weeks 42 and 43, followed by deeper cuts of –20% in Week 45 and –4% in Week 46. If booking momentum stays weak through late October, more cancellations are expected in November.

On the rate front, the Shanghai Containerized Freight Index (SCFI) remained unchanged during Golden Week and will next be updated on October 10. Carriers have announced General Rate Increases (GRIs) for the second half of October to prevent further deterioration, though market sentiment remains hesitant. A second GRI round and additional blank sailings are likely in early November if current efforts fail to gain traction.

Port congestion continues to weigh on operations across key North European gateways.

- Belgium Industrial action by traffic controllers continues to disrupt operations across Antwerp and Zeebrugge, with import handling heavily impacted. Export flows remain stable, but high yard utilisation is compounding congestion.

- Germany Hamburg is operating under pressure - CTA has reduced berth capacity due to terminal reconstruction, while CTB faces up to 7 days of vessel waiting. Wilhelmshaven and Bremerhaven remain tight, with yard utilisation near full and stricter gate restrictions now in place to manage dwell times.

- Southern Europe Congestion persists across Piraeus, Genoa, La Spezia, and Naples, with average waiting times between 2–3 days. Labour shortages in Genoa continue to slow vessel handling, while yard density across Italy remains elevated.

- Netherlands A 48-hour strike at Rotterdam has disrupted container handling and inland transport, with further protests planned that may impact rail movement. Terminal outages and scheduled maintenance at RWG and ECT caused additional operational delays.

- Slovenia At Koper, vessel waiting times average 5 days, with high yard utilisation and extended dwell times. Ongoing rail reconstruction through 2026 is limiting train traffic, pushing more volume onto the roads.

- Spain & UK Valencia and Barcelona are seeing moderate vessel bunching, with delays of 2–3 days and yards over 80% full. In Southampton, delays persist as volume remains high and one berth crane remains out of service, though additional labour is helping clear the backlog.

Ocean freight rates

Capacity and schedule reliability

Europe bottom line

- Demand recovery remains sluggish: Carriers’ pre-holiday overbooking hasn’t translated into stronger post-holiday liftings.

- Blank sailings continue to define strategy: Expect deeper cuts through mid-November if GRIs don’t hold.

- Rate momentum uncertain: Without a meaningful rebound in bookings, pricing will struggle to stabilise.

Global air freight

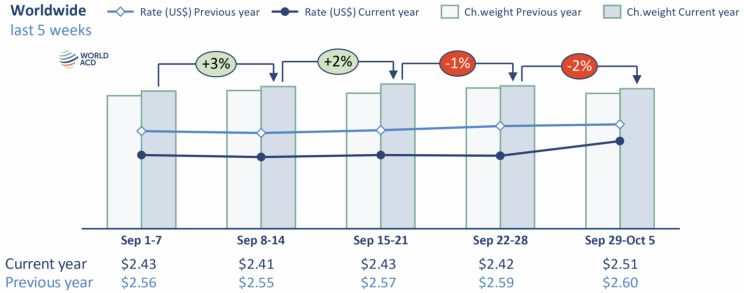

Tonnages from Hong Kong to Europe rebounded sharply: +29 % week-on-week after a storm-induced drop, while China → Europe also saw a modest lift of +6 %. Asia Pacific to USA volumes remain mixed - some markets dipped, others (Vietnam, Malaysia, Thailand) grew strongly. Overall, global rates are under pressure: Asia → USA spot rates are down ~18 % year-on-year, and Asia → Europe down ~11 %, despite rising volumes. Meanwhile, the global average full-market rate ticked up ~3 % WoW to USD 2.51/kg, but is still ~4 % below last year’s levels. Source: World ACD

Global air freight bottom line

- Air cargo volume is bouncing back following disruptions (storms, holidays), but pricing weakness persists across most Asia–West trade lanes.

- Rate recovery is fragile - momentum depends on sustained demand and limited overcapacity.

Global shipping overview

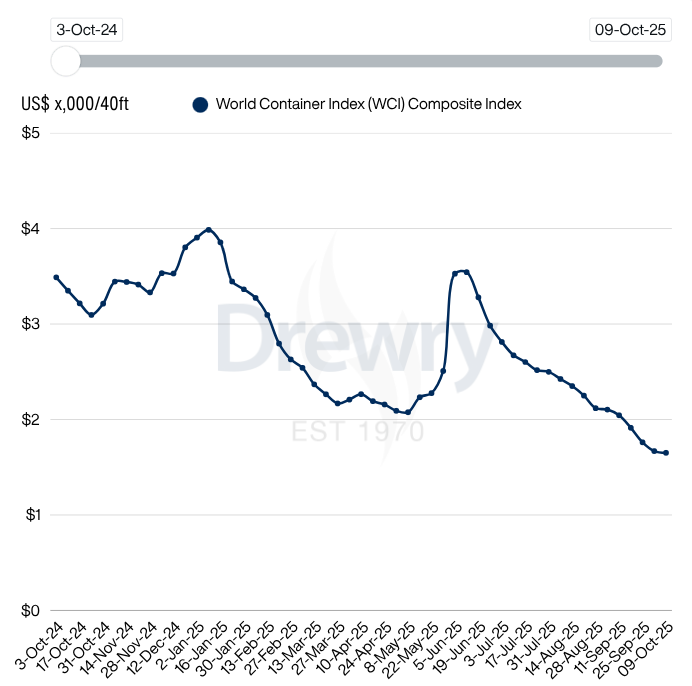

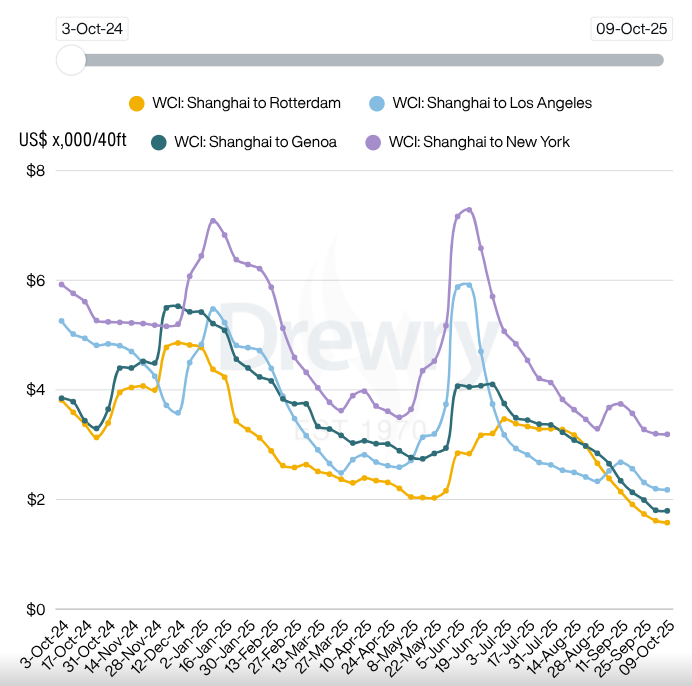

Drewry’s World Container Index fell 1% this week to USD 1,651 per 40-ft container, marking the 17th consecutive weekly decline and the lowest level since January 2024. On the Transpacific route, rates softened slightly, with Shanghai–Los Angeles dipping around 1% while Shanghai–New York held steady. Asia–Europe lanes remain under pressure, with further erosion across both Rotterdam and Genoa corridors. Drewry’s outlook suggests that as the supply–demand balance continues to weaken into Q4, spot rates are likely to contract further despite ongoing capacity controls. Source: Drewry

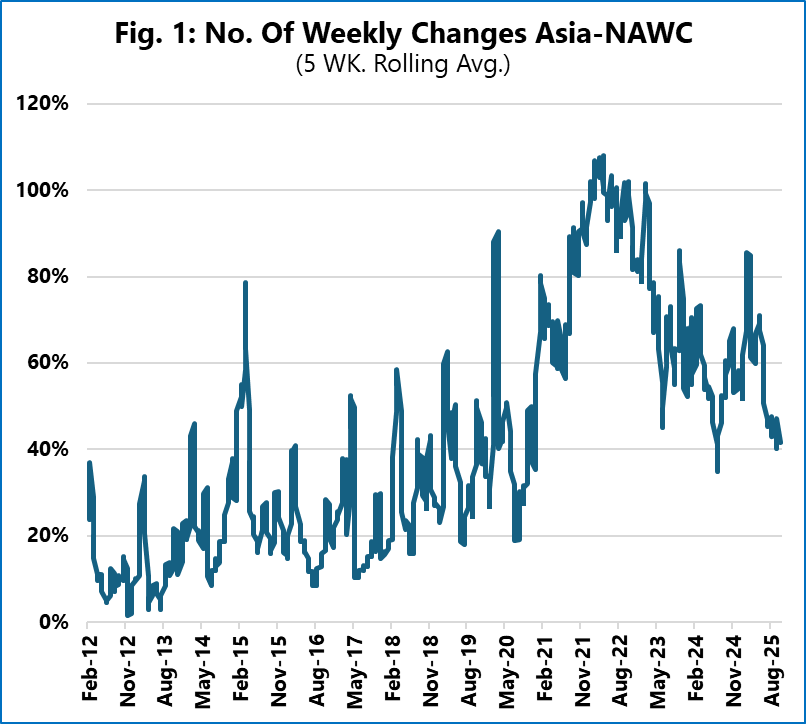

Sea-Intelligence reports that service instability in liner shipping has surged: the frequency of non-standard schedule changes (cancelled or extra sailings) across major trades in 2024–25 is now 2.5 to 3.5 times higher than pre-pandemic levels. On the Asia → North America West Coast trade, average instability now sits at 56%, up from ~23%. Similar structural shifts are seen across Asia → Europe, Asia → Mediterranean, and transatlantic routes. This signals a new normal of unpredictable weekly service changes that undermine schedule reliability and force shippers to absorb more disruption risk.

Global shipping bottom line

For Australian importers and exporters, softer global freight rates bring short-term cost relief, but rising schedule instability is the real risk. Frequent blank sailings, vessel delays, and transshipment congestion are creating unpredictable transit times, especially through Singapore and Port Klang. The market may be cheaper, but it’s also more volatile and operationally fragile.

- Global spot rates remain on a downward trend, with carriers struggling to stabilise pricing despite GRIs and blank sailings.

- Oversupply and muted demand continue to undermine the market, driving rates toward contract parity across key trade lanes.

General news

China’s exports surged 8.3% in September despite heavy tariff pressure, an acceleration largely powered by redirecting shipments from the U.S. toward Europe, ASEAN, Africa, and Latin America. Global demand is evolving: what used to flow through U.S. gateways is now increasingly routed through Southeast Asia, Mexico, and EU markets. This shift weakens the leverage of U.S. tariff strategy, signaling a deeper realignment in global trade networks. Beijing is reinforcing this pivot with infrastructure investments and trade deals to lock in new trading corridors. Source: Global Trade

U.S. Trade Representative Jamieson Greer says whether a sweeping 100% tariff on Chinese exports takes effect November 1 depends squarely on Beijing’s next move. Greer pressed China to roll back its expanded export controls, especially on rare earths, and warned that mixed messaging from Chinese officials is undermining any diplomatic path forward. Source: Reuters

A new hacking group dubbed the Coinbase Cartel has emerged with a clear focus on logistics firms, and DSV has already been targeted. They specialise in data exfiltration, staged leaks, and negotiated extortion - operating like a “professional” cybercrime syndicate rather than random attackers. Source: The Loadstar

Tens of thousands joined a national strike in Brussels as Belgium’s major unions protested government austerity and pension reforms. The walkout crippled air, port, and public transport operations, halting flights at Brussels and Charleroi airports and suspending vessel movements at Antwerp Port, where over 100 ships remain anchored offshore. Workers are opposing plans to raise the pension age and cut unemployment benefits, arguing the reforms unfairly target the middle and working class. The strike, largely peaceful but disruptive, has caused one of the most significant slowdowns in Belgium’s logistics network in recent years. Source: BBC

Interesting Articles

- Global Logistics Surge: International Freight Forwarding Market Set to Surpass USD 167.2 Billion by 2032

- Arctic Sea Route access reshapes global shipping carbon emissions

- How Tariffs Are Helping to Fuel Supply Chain Circularity

.avif)

Experienced Business Development Manager with a demonstrated history of working in the logistics and supply chain industry. Skilled in Import/Export, Freight Transportation, Freight, Warehouse Operations, and Overseas Networking.

Frequently Asked Questions

Explorate gives supply chain managers one real-time view across ever forwarder, lane and mode without replacing your current process, partners or systems.