.png)

What's happening in global freight

Global freight markets are sitting in a mix of tight capacity, weather-driven delays and uneven scheduling. Asia’s major hubs are still managing congestion and vessel bunching, while Europe faces ongoing port delays and inland equipment shortages. Early-November rate hikes on China-Australia lanes have already eased as demand softens into late month.

Global freight trends

.png)

For oceania shippers: Volatility is still the theme. Prioritise space, reliability and lead-time buffers. Expect intermittent delays across Southeast Asia, North Asia and Australia’s east coast as weather, backlog clearance and operational constraints continue through November.

Australia

Australia

Australian shippers continue to experience intermittent disruption driven by a mix of weather-related delays, IT maintenance, and industrial activity across key ports. Heavy rainfall and high winds along the east coast have caused short-term berthing delays in Brisbane and Sydney, while scheduled IT upgrades at DP World terminals have temporarily impacted truck turnaround times.

In Adelaide and Fremantle, occasional work stoppages and restricted operating windows linked to enterprise agreement discussions have added minor congestion during peak hours. Meanwhile, continuing port rotation changes along Australia’s east coast reflect carriers’ efforts to bypass congestion and protect schedule integrity across regional loops.

Overall, disruption levels remain manageable, but importers should allow for a 1–2 day buffer on vessel arrivals and container availability through mid-November.

Sydney

- DP World Port Botany wrapped up its IT and civil infrastructure upgrades in late October with minimal disruption to operations. The next phase of enhancements is already underway, designed to boost terminal efficiency ahead of the 2026 peak season.

- However, the Maritime Union of Australia has confirmed stop-work meetings across all terminals on 25 November, with further industrial action anticipated through the remainder of the year. Shippers should plan for intermittent delays and potential schedule adjustments as negotiations continue.

Melbourne

- Major road and air-freight links progress - the Wurundjeri Way extension is now open as part of the West Gate Tunnel project, introducing new tolling for heavy vehicles, while Avalon Airport launches a 24/7 freight processing facility capable of handling 100,000 tonnes annually with upgraded Border Force-compliant screening.

Adelaide

- Flinders Adelaide Container Terminal begins a $400 million upgrade, including new post-super Panamax cranes (Australia’s largest), berth extensions, and a TOS modernisation program to significantly lift efficiency.

Darwin

- A new 30-year master plan unveiled, targeting capacity growth to 300,000 TEU annually, expanded bulk handling, and integrated rail and road upgrades - positioning the Top End as a strategic trade hub for Northern Australia.

Australia’s key container gateways continue to progress infrastructure upgrades and capacity improvements heading into 2026. The overall outlook remains stable, with several long-term developments designed to enhance efficiency, connectivity, and trade growth across the nation’s ports.

North East Asia

North East Asia

After a strong start to November, the China–Australia trade has entered a sharp correction phase. Carriers, buoyed by high early-month utilisation and strong booking forecasts, pushed for another round of General Rate Increases (GRIs) in the second half of November, but this proved largely unsustainable.

With vessels departing from mid-month set to arrive around Christmas, most shippers have already front-loaded orders, softening demand considerably. As a result, many of the rate hikes introduced after November 15 have been described as “artificial increases”, quickly eroded by a renewed price war among carriers.

Budget and mid-tier operators were the first to break ranks, cutting prices to secure space utilisation as bookings slowed. Meanwhile, premium carriers are holding firm at elevated pricing through November 30, citing significant backlogs and a desire to maintain service reliability over short-term market share.

Ocean freight rates

Rates out of North East Asia have entered a sharp correction phase. The aggressive GRIs introduced after 15 November have proven unsustainable, with softer mid-month demand triggering rapid discounting across budget and mid-tier services.

- Budget Services (CAT, CA2): Now sitting around USD 1,450 per 20GP and USD 2,900 per 40HQ, as carriers cut rates to protect utilisation.

- Mid Tier Services (NEAX/A1X): Have eased to USD 1,550 per 20GP and USD 3,100 per 40HQ, holding only a slight premium as demand stabilises.

- Premium Services (A3C, A3N): Holding at around USD 2,200 per 20GP and USD 4,400 per 40HQ, supported by backlog clearance and stronger reliability commitments through late November.

The widening gap between premium and budget tiers reflects a market now driven by volume protection rather than price discipline.

Capacity and schedule reliability

- Utilisation is softening across East and North China, particularly post-Nov 15, as cargo flow slows ahead of Christmas.

- Market fragmentation is intensifying as carriers fight to retain bookings amid falling demand.

- Premium lanes remain at capacity due to backlog; however, this is expected to ease by early December.

- West Coast services stable but constrained by trans-shipment congestion in Singapore and tight vessel rotations.

In short: Capacity is loosening, reliability is splitting by service tier, and late-November conditions will stay volatile as carriers work to fill remaining space.

South East Asia

South East Asia

.avif)

Over the past two weeks, container flows across Southeast Asia have remained under pressure from moderate demand and persistent operational friction. Capacity injections and blank sailings continue to balance each other, but effective supply remains tighter than headline figures suggest. Key hubs such as the Port of Singapore and Port Klang are seeing yard densities and vessel-queuing that are contributing to service uncertainty.

Ocean freight rates

Rates out of South East Asia remain stable moving into the second half of November.

- The premium services increased by approximately 20%, while the more budget carriers saw little movement.

- Budget to Mid-Tier rates out of Indonesia, Vietnam, and Thailand remained modest in comparison, varying between USD850 - 950 per TEU.

- Singapore, Taiwan, and Malaysia varied between USD1150 - 1300 per TEU.

Capacity and schedule reliability

- Major trans-shipment and direct gateway ports in SEA continue to record berthing and yard delays, driven by vessel bunching, feeder constraints, and the residual impact of weather or accident-related disruptions.

- Schedule reliability remains moderate - importers and exporters should plan for possible 1–2-day delays or booking margins when relying on SEA transshipment hubs feeding Australia.

- Carriers are increasingly omitting Fremantle from their rotations to mitigate ongoing congestion and delays at Singapore.

Asia bottom line

Southeast Asia remains in a mode of managed tension - not high-growth, but constrained enough to keep carriers cautious. For shippers using SEA hubs, the watch words are visibility, buffering, and selective booking discipline rather than rate-chasing or expecting major space relief.

With ongoing congestion, we can expect bottlenecks ahead of the Chinese New Year rush.

North America

North America

Ocean freight rates

After several months of rate escalation, the market is finally stabilising. GRI activity is muted with the November 1 increase softened and no further GRI confirmed for mid-month. PSS has been postponed to December 1.

Capacity restoration and cautious carrier behaviour suggest a more predictable pricing environment through the remainder of November.

Capacity and schedule reliability

The Trans-Pacific trade has entered November with a noticeable rebound in vessel availability. Capacity has increased by 10–15% across all China–U.S. gateways as carriers reposition equipment and reinstate blanked sailings from October. Average utilisation is tracking between 83–88%, with stronger liftings to the U.S. West Coast compared to softer East Coast demand. The earlier tariff rush has now stabilised, leaving a more balanced flow of cargo through mid-month.

- Capacity up 10–15% MoM as carriers reinstate previously blanked sailings.

- Utilisation stronger ex-China to U.S. West Coast than East Coast.

- Delays in container availability from West Coast terminals, with 7-10 days expected during peak season.

- Air Freight: The U.S. federal government shutdown triggered dramatic disruption in aviation, with the Federal Aviation Administration (FAA) requiring airlines to reduce flight capacity at about 40 major airports by up to 10%, and warning that reductions could reach 20% if the impasse continues. Source: CNN

US/Canada bottom line

The Trans-Pacific trade has entered a phase of measured stability after months of volatility. Increased capacity and softened GRIs are bringing rate consistency, while utilisation remains solid (especially to the U.S. West Coast).

However, port dwell times of 7–10 days and the ongoing U.S. government shutdown’s impact on aviation and cargo scheduling could create pockets of disruption. For shippers, this is a moment to consolidate forecasting accuracy, secure allocations early, and focus on service reliability rather than chasing marginal rate gains. The market’s balance is delicate and proactive planning now will protect margins into the new year.

Europe

Europe

.png)

Europe’s container trade continues to operate under a delicate balance of soft demand, lingering congestion, and selective capacity discipline.

On the Far East Westbound (FEWB) lane, utilisation remains subdued at around 85%, as carriers counter weak European import volumes with blank sailings and service suspensions. Meanwhile, the Trans-Atlantic Westbound (TAWB) corridor shows relative stability but ongoing congestion across North and South Europe.

Yard utilisation across major gateways - Rotterdam, Antwerp, Hamburg, and Genoa is averaging 75–89%, with berth delays of two to seven days and mounting dwell times. Persistent congestion at key Northern European hubs has reduced round-voyage frequency by up to 30%, absorbing excess capacity but leaving operations strained.

Ocean freight rates

- Carriers are holding rates steady through deliberate capacity control.

Capacity and schedule reliability

- FEWB utilisation is hovering at ~85%, below seasonal norms; selective blank sailings offset excess supply.

- North European congestion persists: Rotterdam 9 days, Antwerp/Hamburg 3–5 days, cutting round-voyage frequency by up to 30%.

- TAWB networks are affected by inland equipment shortages across Austria, Hungary, and Southern Germany, slowing container repositioning.

- Weather and labour constraints are expected to sustain moderate delays through December.

The European market is characterised by artificial tightness rather than strong demand. Congestion and equipment shortages have absorbed spare capacity, temporarily supporting rate stability. As winter sets in, demand softens further, and carriers are likely to maintain controlled capacity and disciplined pricing through year-end.

Europe bottom line

For shippers, this means longer lead times, reduced flexibility, and limited space fluidity even as overall demand softens. Expect the region to stay in a “managed stability” phase through December, where carriers prioritise cost discipline and service integrity over volume growth. Importers and exporters should focus on precision planning and proactive coordination to maintain consistency through the winter slowdown.

Global air freight

In week 44, global air-cargo tonnages slipped by about -3% versus the previous week, yet average spot rates continued a slight upward trajectory, indicating capacity pressure despite softening volume. While overall volumes remain broadly flat year-on-year for many origin markets, the mix of trade lanes is shifting - with notable volume rebounds on select Asia-Pacific to North America and Africa to Europe routes. Meanwhile, capacity across passenger-belly and dedicated freighter services remains elevated in many regions, limiting the upside for rates.

Airfreight space from China into Australia remains tight but improving across most gateways, with additional capacity gradually opening from 12–18 November.

Overall, South China remains the most constrained, particularly for multi-leg routings via Singapore and Kuala Lumpur. Several carriers have reinstated limited frequencies, but space on second legs remains under pressure. Rates are mixed - largely stable ex-PVG and CAN, with modest increases ex-PEK and HKG/SZX where demand for e-commerce and heavy cargo remains strong.

Global air freight bottom line

The air-cargo market entering November is not overheated but is braced for selective tightness. Shippers focused on high-value, time-sensitive cargo have the upper hand - but the general-demand environment remains moderate. For customers in Australia, this means: ensure you have contingency for top-priority shipments, but don’t overspend on air freight as a blanket solution. Use this window to cleanse your data, refine your prioritisation criteria, and build strong carrier relationships ahead of Q1 contract season when demand may pick up again.

- Overall trend: Airfreight demand remains steady ex-China, with selective rate adjustments and improving capacity from mid-November.

- Tightest lanes: South China → Sydney/Melbourne via Singapore and Kuala Lumpur.

- Carrier behaviour: Most airlines prioritising high-yield, dense, or heavy cargo; some offering promotional rates for light or volumetric goods.

- Outlook: Expect gradual easing of space constraints as mid-month frequencies increase, but pre-Christmas demand could again tighten capacity by late November.

Global market overview

Global container-freight markets continue to operate under muted demand, with the recent easing of U.S.–China trade tensions reducing one key source of volatility.

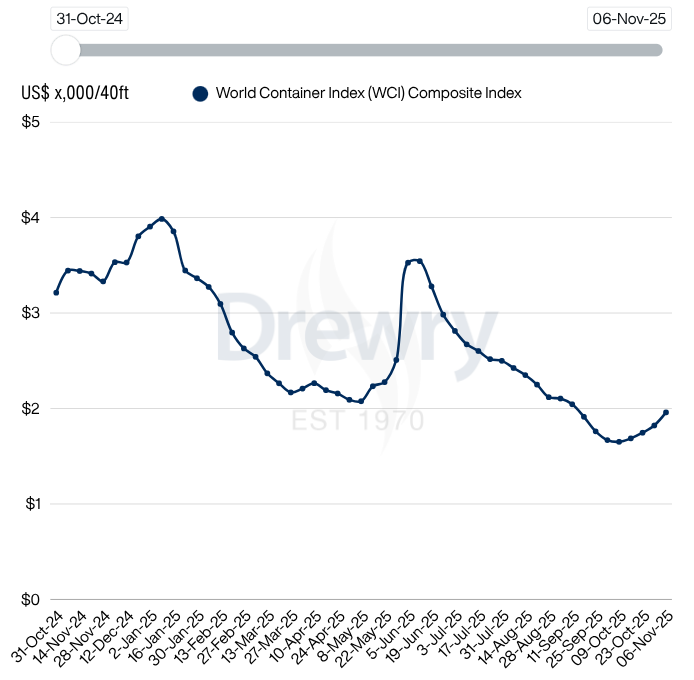

Freight rates

The World Container Index rose 8% last week to USD 1,959 per 40-ft container, marking the first meaningful uptick after 17 consecutive weeks of decline. The rebound reflects short-term carrier discipline and strategic rate restoration rather than a genuine recovery in global trade volumes. Drewry notes that the overall supply-demand environment remains weak, and any sustained momentum will depend on continued blank sailings or early peak-season restocking

- Asia → North America Rates from Shanghai to Los Angeles increased around 9% to USD 2,647 per FEU, while Shanghai to New York rose 8% to USD 3,837 per FEU. The uplift is largely driven by recent General Rate Increases (GRIs) applied by major carriers to stabilise the Trans-Pacific market.

- Asia → Europe Rates from Shanghai to Rotterdam climbed 9% to roughly USD 1,962 per FEU, and Shanghai to Genoa rose 8% to about USD 2,111 per FEU. Despite low import demand in Europe, carriers have introduced FAK (Freight All Kinds) rates between USD 3,000–3,600 for November–December shipments to support a pricing floor.

- Other / Reverse Lanes: Rate trends remain largely flat across secondary corridors. Carriers are expected to maintain moderate capacity reductions to prevent renewed downward pressure.

Schedule reliability

- Although congestion at major nodes persists (thereby limiting available effective capacity), the absence of significant freight-rate upward momentum suggests that carriers are prioritising preserving utilisation and service integrity over aggressive yield improvement.

- Service deployments remain relatively stable, but with extended dock and yard delays in Europe and some equipment/repositioning constraints elsewhere, shippers should anticipate incremental reliability risks ahead of the traditional winter downturn.

Global shipping bottom line

- The short-term rate rebound indicates that carriers are testing the market and attempting to hold pricing through controlled capacity and GRIs.

- Asia-to-US and Asia-to-Europe lanes show the most resilience, suggesting that shippers should not rely on further spot-rate declines in the near term.

- The current uptick is strategic rather than demand-driven; unless booking volumes improve, the market could see another correction before year-end.

- For procurement and supply-chain teams, this is a signal to secure short-term stability rather than chase further reductions - especially ahead of Q1 2026 contract discussions.

General news

- The ongoing U.S. federal government shutdown has escalated into a significant operational crisis for aviation. With the Federal Aviation Administration (FAA) citing mounting fatigue among air-traffic controllers, many of whom are working without pay or have reported for overtime after missed paychecks, the agency has mandated progressive flight-capacity cuts at 40 major airports. Initially ordering a 4% reduction in scheduled flights starting early November, the directive is set to scale up to 10% by November 14, and could reach as high as 20% if the shutdown persists. Airlines are already experiencing thousands of cancellations and hours of delays, and cargo operations are not immune - the ripple effect threatens air-freight capacity, routing flexibility, and premium-rate exposure as importers and exporters brace for restricted belly-hold and dedicated cargo space. Source: CNN

- Asia’s transport-and-logistics sector is navigating a blend of structural shift and operational stress - while carriers and exporters brace for softer export demand, particularly from China, new routes and modalities (like Arctic and land-rail corridors) are emerging amid geopolitical realignments. Congestion, regulatory uncertainty and capacity mismatches remain central challenges, forcing shippers and ports to prioritise visibility and flexibility over volume expansion. Source: Reuters

- The ultra-large container ship CMA CGM Benjamin Franklin has successfully transited the Red Sea and entered the eastern Arabian Sea, marking the first ULC return to the Suez‐route corridor by the CMA CGM alliance since disruptions began in late 2023. This voyage is seen as a strategic “test” of the route’s viability amid ongoing security risks from Houthi activity, rather than a full-scale return to the Red Sea. While the move signals carriers are quietly preparing for the corridor’s reopening, they remain cautious about sending more vessels until the operational and geopolitical environment stabilises. Source: Lloyds List

.avif)

Experienced Business Development Manager with a demonstrated history of working in the logistics and supply chain industry. Skilled in Import/Export, Freight Transportation, Freight, Warehouse Operations, and Overseas Networking.

Frequently Asked Questions

Explorate gives supply chain managers one real-time view across ever forwarder, lane and mode without replacing your current process, partners or systems.