.avif)

Australia

Australia

Brisbane

We have been notified of a terminal shutdown at the Patrick Fisherman Islands Terminal. All ship and yard operations will cease between 0700 - 1500hrs on Sunday 13th July 2025.

Sydney

A powerful "bomb cyclone" rolled into Sydney on the afternoon of 1 July, bringing destructive winds (up to 125km/h), torrential rain, and heavy swells. The Bureau of Meteorology issued strong warnings, with conditions expected to ease by Thursday, 3 July. As a result, all vessels were secured on storm lines, and port operations were brought to a standstill—no loading, no unloading. Empty parks were closed, and several ships bypassed Sydney altogether, adding pressure to already strained terminal operations. Delays and congestion are expected to ripple through the week.

Melbourne

Due to strong winds currently affecting Victoria, several Melbourne empty container depots are experiencing intermittent closures.

Fremantle

With wild weather on the horizon from 6–8 July, vessels off Fremantle were sent out to sea for safety. In response to the conditions, DP World confirmed it would pause operations from 2:00 PM Sunday, 6 July, through to 6:00 AM Monday, 7 July. Safety first as the port braces for the impact.

Flinders Adelaide Container Terminal (FACT):

South Australia's sole container terminal since 1978, is undergoing a significant $350 million upgrade to enhance capacity and efficiency over the next three years. Key enhancements include:

- Berth Expansion: A 135-meter extension to Berth 6 will enable the terminal to accommodate two 366-meter vessels simultaneously.

- New Cranes: Installation of two Super Post Panamax Ship-to-Shore (STS) cranes, expected by early 2027, will boost cargo handling capabilities.

- Empty Container Depot Expansion: Doubling the depot's capacity, including over 100 reefer points, to better serve shipping lines and transport companies.

- Infrastructure Upgrades: Implementation of advanced gate technology, upgraded IT systems (TOS, DOS, VBS), and new site-wide services to streamline operations.

- Automation Trials: Testing of an Automated Rubber Tyred Gantry (ARTG) system to increase operational efficiency. Source: The DCN

Biosecurity Costs:

On June 30th, AQIS released ACN 2025/16 to outline that as of 1 July 2025, there will be changes to the biosecurity cost recovery charge on Full Import Declarations (FIDs) for goods arriving in Australia by air and sea.

As tabled below, the changes to the current charges will apply to imports from 1 July 2025.

In addition, the current charges for import cargo documentation for assessment through COLS will increase from $39 to $40 in line with the Department’s Cost Recovery Implementation statement (CRIS).

Further information > Fees and charges for biosecurity regulatory activity from 1 July 2024

North East Asia

North East Asia

- The Asia-Pacific market is messy right now, and space remains a challenge across the board. Penang is still a headache. Ex-China space is tight, with A3 services seeing around a week’s delay just to secure a booking. Vessel delays arriving into China are also pushing ETDs out, so planning has become a moving target.

- Vietnam, especially Haiphong, isn’t faring much better. We’re seeing bookings confirmed and then last-minute vessel delays come through, throwing things off track. Transhipment hubs like Singapore and Port Klang are still unreliable - vessel delays with no solid information, and often, no assigned transhipment vessel at all. That makes giving clients a realistic ETA tricky. We're constantly monitoring schedules daily, just to keep updates accurate.

- On the carrier side, many have pulled back their earlier rate increases as pressure mounts from the flood of large vessels scheduled later this month. Those without solid long-term contract support are feeling it most. There’s been a round of downward adjustments to stimulate volume, especially out of South China ports like Shenzhen and the Pearl River Delta. Northern ports, like Dalian and Tianjin, remain more stable, but space is limited, so they’re less volatile right now.

- Looking ahead to August, we’re definitely heading into the true peak season. Early signs point to rates increasing again, and while some of the published numbers seem ambitious, rate hikes are expected. We’ll have a clearer picture in the coming week.

Ocean freight rates

Aggressive Rate Hikes: Major carriers (including OOCL, ANL, COSCO, PIL, and MSC) issued substantial Peak Season Surcharges (PSS), typically targeting USD 500.00 per TEU. Rates were projected to climb above USD 1,300.00 per TEU by mid-July, with carriers aggressively eyeing USD 1,600.00 per TEU by August 1st.

Capacity and schedule reliability

Capacity & Blank Sailings

Carriers utilized aggressive blank sailings to systematically choke out market overcapacity:

- CA2 Service: Scheduled a blank sailing in early July (Week 27), wiping out 4,200 TEUs of capacity across Qingdao, Shanghai, and Shenzhen departures.

- CAT Service: Executed an early July (Week 27) blank sailing, removing 5,000 TEUs of capacity from Shanghai, Ningbo, and Shenzhen.

- A3S Service: Hit mid-July (Week 28) with a blank sailing, slashing 5,500 TEUs of capacity across Xiamen, Hong Kong, and Shenzhen loops.

- Wallaby Service (MSC): Planned a blank sailing for late July (Week 30) impacting Shanghai, Xiamen, Hong Kong, and Shenzhen departures.

Capacity Reductions: MSC strategically shifted several large 9,000 TEU vessels off the route, replacing them with smaller 6,000 TEU ships, which effectively lowered overall capacity on the China-Australia trade lane and drove up spot rate sentiment.

Peak Season Timing: Cargo volumes saw a major spike in late July due to a combination of post-fiscal year order releases and early peak-season momentum.

Port Congestion & Delays

- Shanghai: Faced intense vessel delays of up to 3 days due to heavy port congestion and seasonal sea fog, significantly disrupting schedule transit times.

- Ningbo: Average vessel wait times hovered around 2 days, with growing container roll pools stemming directly from the blank sailing cutbacks.

- Qingdao: Severe weather-related pileups forced vessels to wait an average of 2 days before securing an open berth.

South East Asia

South East Asia

.avif)

Ocean freight rates

- Rate Increases: Freight rates on core lanes heading out of key Southeast Asian hubs jumped across the board for the second half of July.

- Singapore, Malaysia, & Indonesia: Rates surged by approximately 10%. Due to extreme space limitations at the high end of the market, prices showed massive variance, floating anywhere from USD 850.00 to an expensive USD 1,500 per TEU.

- Thailand & Vietnam: Registered steady marginal rate increases between 10% and 15%, with active spot rates landing within the USD 950.00 to 1,550 per TEU spectrum.

- Fremantle & Adelaide (West Coast Trade): While the direct trade structure remained unchanged, the rampant transhipment logjams in Singapore forced rates to settle into a rolled-over slot ranging between USD 800.00 and 1,350 per TEU.

Rate Summary: 15th July - 31st July 2025

Most Competitive Services:

Budget carriers such as CAT and CA2 have offered a final rate of approximately USD 1,250 per TEU. Maersk has re-entered the market, signalling interest in renewed collaboration. They have extended a preferential spot rate of USD 1,200 per TEU. These rates apply from China Main Ports (CMP) to Australia's East Coast (AUEC), valid for cargo loaded between 15th and 31st July.

Mid-Tier Services:

The NEAX (A1X) & ZAX/Wallaby services currently have set rates at between USD 1,250-1300 per TEU. Their vessels filled up ahead of official rate announcements, suggesting that strong demand will keep rates firm through the end of July.

Premium Services:

Leading premium service providers continue to set the tone for the market with their clear, confident, and decisive pricing strategies. Their strong market position allows them to take the lead, with many other carriers typically following suit when adjusting their own rate levels.

For the second half of July, these carriers have set rates at USD 1,400 per TEU. These benchmark figures are expected to influence broader market pricing in the weeks ahead.

West Coast:

The Fremantle/Adelaide (FRE/ADL) trade has remained unchanged since April, with no vessel adjustments or service updates. Despite ongoing volatility on the Australian East Coast (AUEC), carriers have opted to roll over current rates through July. Rates vary from USD800 - 1350 per TEU for the remainder of July.

Advertised GRIs:

ANL: USD350.00 per TEU Peak Season Surcharge (PSS) for all shipments effective 1st August 2025, ex North & South East Asia to New Zealand.

ANL: USD300.00 per TEU for all cargo ex Northeast Asia to Australia & NZ. Effective from 15th July.

MSC: USD300.00 per TEU Peak Season Surcharge (PSS) for all cargo ex China, Hong Kong, Taiwan, Japan, Korea, Cambodia, Thailand, Vietnam, Malaysia, Myanmar, Singapore, Philippines and Indonesia to Australia and New Zealand. Applicable from the 15th July.

MSC: USD500.00 per TEU for all cargo ex China, Hong Kong, Japan, Korea, and Taiwan to Australia and New Zealand. Applicable from the 15th July.

Capacity and schedule reliability

Port & Transhipment Logjams

- Singapore Hub: Remained a critical bottleneck in the network. Average vessel wait times reached up to 2 days, and backlogged transhipment containers were stuck sitting in roll pools for up to 2 weeks.

- Port Klang & Penang (Malaysia): High local demand combined with persistent vessel bunching resulted in 3-day vessel delays. Terminal yards became heavily congested, and major carriers like COSCO and PIL reported being completely booked out through the end of July.

- Vietnam (Ho Chi Minh & Haiphong): High terminal yard utilization hit 80–90% capacity. The severe yard density began limiting landside productivity, leaving ocean carriers grappling with 1-day berthing delays.

India Subcontinent

India Subcontinent

.png)

India – Disruptions Due to Statewide Transport Strike

At Nhava Sheva (Jawaharlal Nehru Port), cargo movement has been disrupted by a statewide truck driver strike in Maharashtra, which began on 2 July. The industrial action is affecting pickup and delivery operations across the region. Logistics providers like Kuehne+Nagel are working to reroute and minimise delays, but ongoing disruptions are expected if the strike continues.

Bangladesh – Congestion and Delays Across Key Facilities

Bangladesh’s supply chain has been strained following a brief but impactful customs officer strike, initially announced by the National Board of Revenue Reform and Unity Council. Although operations have resumed, the temporary halt has left a backlog at CFSs and Chittagong Port.

- Chittagong (Chattogram): Ongoing berthing congestion is causing average vessel wait times of 5–7 days, with port stays now stretching 3–4 days. Seasonal monsoon conditions are also intermittently impacting terminal operations.

- Dhaka Kamalapur ICD: Locomotive shortages have pushed dwell times to 7–10 days for 20’ containers and 2–3 days for 40’ containers. Heavier 20ST containers (over 25 tonnes) face delays exceeding 15 days. Only two trains are currently servicing the Chittagong–Dhaka corridor.

- Pangaon Container Terminal: Import dwell times have increased significantly, now ranging between 1 and 2 weeks, adding pressure to inland movement capacity.

Sri Lanka – Transhipment Delays and Weather Impacts

At Colombo Port, vessel bunching is affecting schedule reliability. Ships arriving on time (“on-window”) are typically berthed within 24 hours, but off-window vessels may wait up to 3 days. Inter-terminal transfers are suffering, with transhipment cargo - especially from Pakistan, Bangladesh, and South India - experiencing prolonged delays. The impact of June’s adverse weather is still lingering in the system.

North America

North America

Ocean rates

Spot (floating) freight rates to the U.S. West Coast continue to slide, now meeting or even dipping below fixed contract levels. The complete removal of the Peak Season Surcharge (PSS) for West Coast shipments starting July 1 reflects the easing of demand pressure. On the East Coast and Gulf routes, floating rates are still holding above contract rates, though the PSS has been scaled back.

Spot rates continue to ease on Trans-Pacific routes.

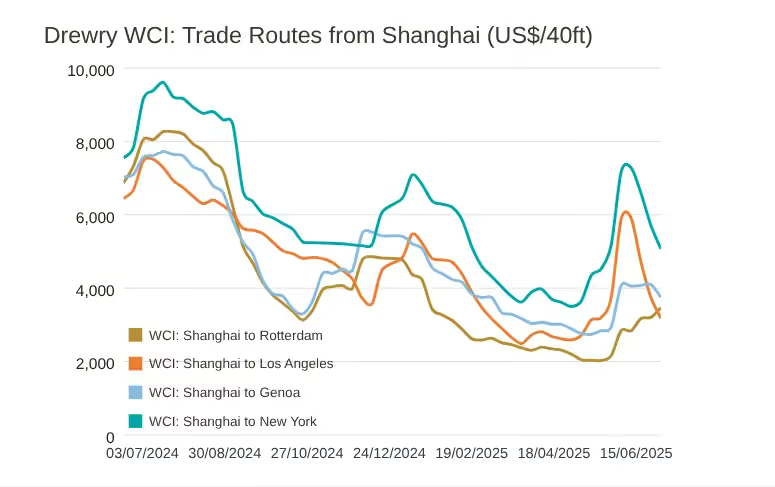

- Shanghai to Los Angeles rates fell by 15% this past week, landing at $3,180 per 40ft container. Despite the drop, rates are still up 17% compared to early May.

- Shanghai to New York saw an 11% decrease, with current spot rates at $5,070, though still 39% higher than eight weeks ago.

Drewry forecasts further declines next week, driven by soft demand and excess capacity on US-bound services. Source: Drewry

Capacity

- Overall capacity is sitting at a high 84–91%, indicating an oversupplied market relative to the current demand levels. Carriers are maintaining flexibility with ad-hoc blank sailings rather than implementing wide-scale service cuts. Equipment availability across key origin ports is steady, showing no major shortages - further evidence of a well-supplied network.

- In May 2025, the Port of New York and New Jersey (PANYNJ) emerged as the busiest seaport in the United States, processing 774,698 twenty-foot equivalent units (TEUs). This volume reflects a 20% increase compared to May 2019, though it represents a slight 2% decrease from May 2024, a month that experienced an unusual surge due to cargo rerouted from the Port of Baltimore following the collapse of the Francis Scott Key Bridge From January through May 2025, PANYNJ handled a total of 3,729,611 TEUs, marking a 6.5% increase over the same period in 2024 and a 22.6% rise compared to the first five months of 2019. This growth underscores the port's resilience and adaptability amid shifting trade dynamics and tariff-related uncertainties. Source: Maritime Executive

Schedule Reliability

- With July volumes expected to stay flat, there's no significant post-Q2 surge anticipated. This suggests a slowdown following the pre-tariff rush seen earlier. While carriers aren’t aggressively pulling services, the sporadic nature of blank sailings suggests they’re making week-to-week adjustments to balance supply with weaker demand.

US Tariffs

Key updates (as at 9 July 2025):

- New U.S. tariffs delayed to 1 August

- Planned tariffs: 25–40% on 14 countries including Japan, South Korea, Thailand

- Market volatility follows tariff news

- De minimis crackdown and phase-out by 2027

- Vietnam trade deal signed – includes transshipment penalties

- EU and UK trade talks ongoing ahead of August deadline

- SHIPS for America Act targets maritime self-sufficiency

👉 Read the full update in our Dedicated Tariffs Blog.

Europe

Europe

.png)

Ocean freight rates

Movement was mixed across Asia–Europe tradelanes.

- Shanghai to Genoa rates fell by 9% to $3,751 per 40ft container.

- In contrast, Shanghai to Rotterdam rates rose 8%, reaching $3,468 per 40ft.

These fluctuations reflect ongoing imbalances between capacity deployment and regional demand trends. Source: Drewry

Despite an overall soft rate environment this year, FEWB carriers are holding firm on July's General Rate Increases (GRIs). Average rates for 40ft containers remain elevated, with no notable drop in the first half of the month. Strong vessel utilization - often booked out 2–3 weeks in advance - is allowing carriers to maintain these levels. So while demand isn’t weak, it’s the surplus of capacity that’s been keeping overall rate growth in check.

Capacity and schedule reliability

Capacity

July has seen a notable capacity injection, with average weekly space up 11% from June, hitting approximately 293,700 TEUs. However, deployments have varied week to week - some weeks spiking above 320,000 TEUs and others dipping to as low as 220,000 TEUs. These swings suggest carriers are trying to shape demand timing, especially in preparation for the peak shipping push in late July and August.

Antwerp & Rotterdam (Belgium/Netherlands):

Terminals are under pressure from high yard density, strikes, staff shortages, and ongoing construction. Barge delays at some terminals exceed 96 hours, and summer holidays may stretch labour availability for up to 10 weeks.

Hamburg & Bremerhaven (Germany):

Yard space is maxed out. Bremerhaven is seeing berth waiting times of nearly 3 days, while Hamburg terminals (CTA, CTB, CTT) are grappling with delayed vessels, tight yard space, and gate-in restrictions.

Algeciras (Spain):

High yard density and full berthing lineups persist. Some vessels face a 2-day wait.

Genoa (Italy):

Congestion remains an issue, with an 84% yard fill rate and continued labour shortages.

Valencia (Spain):

Backlogs have cleared, but July construction at APMT will impact gate and rail operations.

Schedule reliability

The inconsistent weekly capacity has created friction in the network, leading to higher rollover incidents and pockets of equipment shortages at origin. Demand remains on a typical seasonal upswing, especially with European retailers stocking early for the holidays. Since March, Asia-to-Europe export volumes have consistently outpaced 2023 levels, supporting a strong market backdrop even amid operational volatility.

European importers are grappling with significant backlogs as rail delays intensify existing congestion at major German ports. Disruptions in both port and rail infrastructure have led to fully utilized berthing line-ups and overcrowded yards, causing substantial delays in cargo movement. This situation is exacerbating the already pressing challenges in the supply chain, making it increasingly difficult for importers to receive goods in a timely manner. Source: The Loadstar

Germany:

Severe rail delays due to infrastructure issues, bushfires near Hamburg, storm damage, and construction closures (notably to Hamburg Waltershof from 4–8 July). Metrans reports delays up to 3 weeks in bookings, partial train handling, and some cancelled services.

Slovenia & Croatia:

Derailments and track failures are disrupting Metrans services to/from the Adriatic and Central Europe. Croatia’s Andrijevci station incident has hit rail flows to/from Rijeka.

Rhine River:

Low water levels from hot, dry weather are restricting barge capacity inland via Rotterdam and Antwerp.

Hamburg (Germany):

- CTB: Vessels arriving outside window are causing 4-day waits; customs clearance paused from 4–8 July.

- CTA & CTT: Facing high yard density and restricted gate-ins. Delays vary from 16 hours to several days.

Bremerhaven (Germany):

A switch failure near Bremen has led to a train bottleneck - only one train per hour permitted.

Rotterdam (Netherlands):

ECT, RWG, Delta II: Barge delays range from 36 to 96 hours. Labour shortages and IT issues are limiting throughput.

London Gateway (UK):

Power outages and late arrivals are creating berth congestion, although yard usage remains moderate.

Algeciras (Spain):

The port is prioritising heavy export vessels to ease congestion.

Valencia (Spain):

Normal operations have resumed, aside from the APMT works.

Global air freight

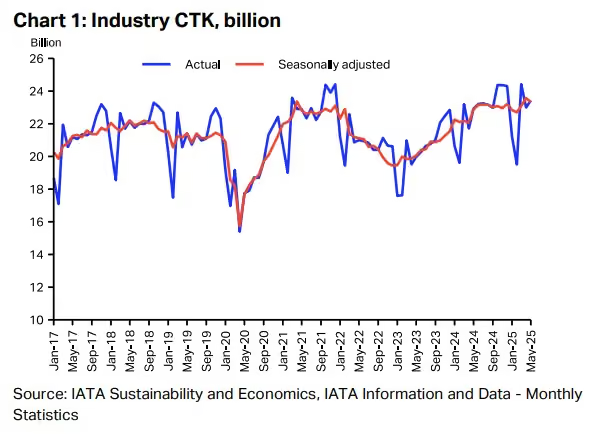

- In May 2025, the global air cargo industry experienced a 2.2% year-on-year increase in demand, measured in cargo tonne-kilometers (CTK). This growth, while positive, marked a deceleration from April's 5.8% rise, attributed to the diminishing impact of preemptive shipping ahead of anticipated tariff implementations.

- International air cargo demand grew by 3.0% compared to the previous year, with the Asia-Pacific region leading at an 8.2% increase. Conversely, the Asia–North America trade lane saw a significant 10.7% decline, influenced by the removal of the de minimis exception and heightened tariffs.

- Capacity, assessed in available cargo tonne-kilometers (ACTK), expanded by 2.0% year-on-year, aligning with the recovery in passenger services and the return of bellyhold capacity.

- Despite challenges such as shifting trade policies and geopolitical uncertainties, the air cargo sector demonstrated resilience, adapting to evolving supply chain demands. The sector's ability to navigate these complexities underscores its vital role in global trade and logistics.

- For a comprehensive analysis, refer to the full IATA report: Air Cargo Market Analysis – May 2025.

- From 26 October 2025, Cathay Pacific is ramping up its services out of Australia, lifting Brisbane - Hong Kong flights to 14 per week and giving Perth the same boost. More frequency means more cargo space, better flexibility, and stronger links into Asia. Source: Cathay Pacific

- And Qantas Freight isn’t sitting still either, kicking off direct freighter services between Sydney and Shanghai from 26 June 2025. With Red Tail A330s flying twice weekly (Thursdays and Saturdays), it’s the first time we’ve seen a regular lane between these two major cargo corridors. A solid win for capacity and transit time. Source: Qantas

- Airside just got a little busier—and a whole lot more efficient. ✈️

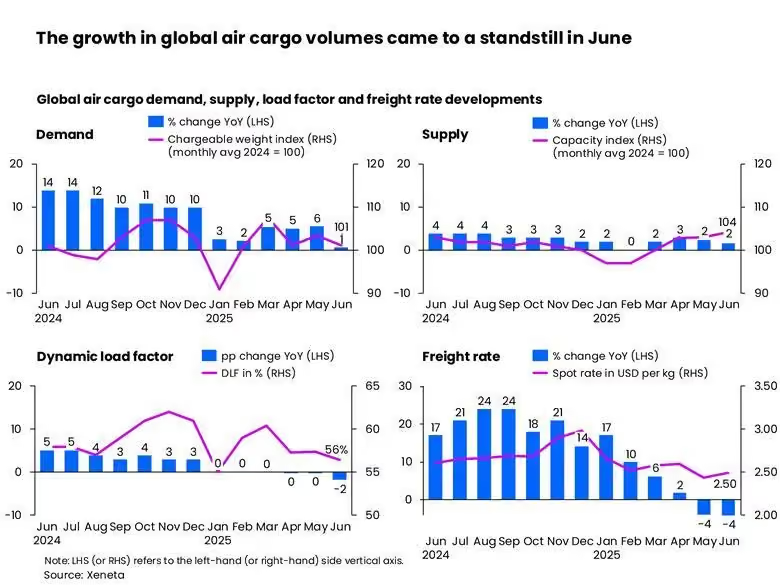

- In June, global air cargo volumes remained stagnant as consumer demand softened, according to Xeneta's latest market analysis. This plateau in volumes is attributed to reduced consumer spending, leading to cautious inventory management by retailers and a slowdown in restocking activities. Despite the stable volumes, the market faces challenges due to excess capacity, which continues to exert downward pressure on freight rates. This situation underscores the ongoing imbalance between supply and demand in the air cargo industry. Source: Air Cargo News

Global shipping overview

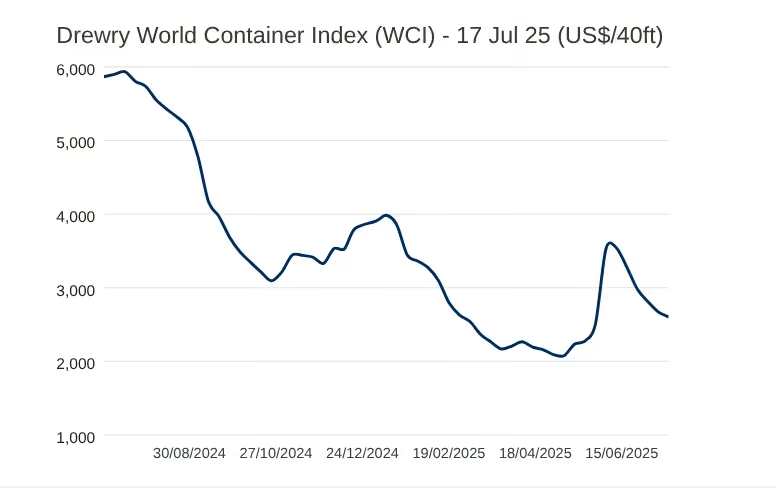

Drewry’s World Container Index (WCI) dropped another 2.6% this week, marking the fifth straight week of declines. This sustained downturn follows a volatile period sparked by higher U.S. tariffs announced back in April. Rates began climbing about a month later, peaking in early June. But that surge didn’t last—since mid-June, rates have been steadily falling, suggesting the initial impact of the tariffs has now faded. Source: Drewry

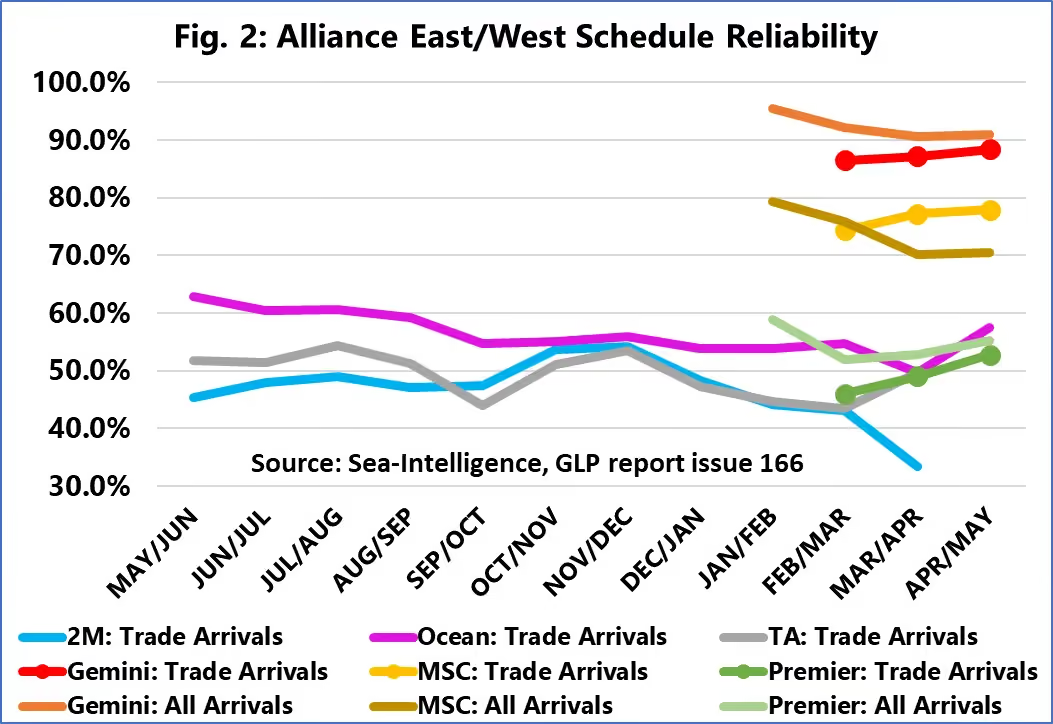

- In April and May 2025, Gemini Cooperation led the industry with a schedule reliability of 90.9% across all arrivals and 88.4% for trade lane-specific arrivals. MSC followed with 70.5% for all arrivals and 77.9% on trade lanes. Premier Alliance trailed behind, posting 55.2% for all arrivals and 52.7% for trade arrivals. For legacy alliances, where "all arrivals" align with trade lane arrivals, Ocean Alliance achieved a reliability score of 57.4%. It's worth noting, however, that the new alliance structures will only be fully implemented by July 2025, at which point a more accurate assessment of their performance can be made. Source: Sea Intelligence

General news

On July 6, 2025, Israel conducted airstrikes on Houthi-controlled ports and infrastructure in Yemen, marking its first such action in nearly a month. The targeted locations included the ports of Hodeidah, Ras Isa, and Salif, as well as the Ras Qantib power plant. These strikes were in response to repeated Houthi attacks against Israel, including a recent assault on the Greek-owned, Liberian-flagged bulk carrier Magic Seas in the Red Sea. The vessel was attacked by rocket-propelled grenades and bomb-laden drone boats, forcing the crew to abandon ship after it caught fire and took on water. Israel also targeted the Galaxy Leader ship at Ras Isa port, which had been seized by the Houthis in late 2023 and reportedly modified with a radar system to monitor maritime activity.

In retaliation, the Houthis launched a missile toward Israel, which reportedly caused no injuries. This escalation follows an earlier incident the same day in which a vessel near Hodeidah came under attack and began taking on water, forcing the crew to abandon ship. While no group claimed responsibility for that attack, security firm Ambrey noted the vessel matched the pattern of typical Houthi targets. Source: GCaptain

Sea robbery incidents in the Singapore Strait have surged dramatically in 2025, with 81 reported cases so far—four times higher than the same period last year. This uptick marks a troubling escalation in maritime security concerns along one of the world's busiest shipping routes.

Key Developments

- Recent Attacks: On July 1, three bulk carriers were boarded within a three-hour window while transiting the Philip Channel. In one incident, perpetrators were reportedly armed with "gun-like" objects. Fortunately, no crew injuries were reported.

- Hotspot Identified: The Philip Channel, particularly its eastbound lane, has become a focal point for these crimes. Vessels often reduce speed in this area, making them more vulnerable to boarding.

- Perpetrators' Tactics: Multiple groups are believed to be operating in the region, often targeting ships during nighttime hours. Their primary aim appears to be theft of ship equipment and crew belongings, rather than cargo.

- Security Recommendations: Authorities, including the ReCAAP Information Sharing Centre, urge ships to enhance vigilance, especially when transiting the Philip Channel at night. They also recommend immediate reporting of incidents and advise against confronting the perpetrators. Source: Seatrade Maritime

Historic flooding in Kerrville, Texas, has resulted in multiple fatalities and significant damage. The severe weather has overwhelmed emergency services, leading to ongoing search and rescue operations. Authorities are urging residents to stay alert and follow safety advisories as the situation develops. Source: NBC News

Interesting Articles

- FTA, CTAA rue Silk decision

- Asia-NAWC capacity volatility more than triples

- The SHIPS for America Act: What It Does and How It Could Change America’s Position in Global Shipping

- European importers face backlogs as rail delays exacerbate port congestion

- What are the key items in Trump's sprawling budget bill?

.avif)

Experienced Business Development Manager with a demonstrated history of working in the logistics and supply chain industry. Skilled in Import/Export, Freight Transportation, Freight, Warehouse Operations, and Overseas Networking.

Frequently Asked Questions

Explorate gives supply chain managers one real-time view across ever forwarder, lane and mode without replacing your current process, partners or systems.