Back to Top

.avif)

Asia

North East Asia

Ocean freight rates

- March 1st GRIs (General Rate Increases) have started to be released. Capacity will need to be cut in order for the increases to hold firm.

- OOCL has announced a rate restoration of USD 200.00 per TEU for all cargo ex Northeast Asia to Australia.

- MSC announced a rate restoration of USD 250.00 per TEU for all cargo ex China, Hong Kong, Japan, Korea, Taiwan, Cambodia, Indonesia, Malaysia, Myanmar, Philippines, Singapore, Thailand, and Vietnam to Australia. They subsequently revised this quantum to USD500.00 per TEU on the 18th Feb. This will still take effect on the 1st March.

- Hapag Lloyd has announced a rate restoration of USD 300.00 per TEU for all cargo ex North and Southeast Asia to Oceania.

- ANL has announced a rate restoration of USD200.00 per TEU for all cargo ex Northeast Asia to Australia East Coast.

- Spot rates post-Chinese New Year have been fluid. Carriers are making changes almost daily ahead of the end of the month.

- The CAT/NEAX services offer the most competitive options, with levels out of base port China sitting at USD 600-700 per TEU into AUEC.

- The A3 service remains slightly higher at USD 800-900 per TEU into AUEC.

- Southeast Asia pricing has also reduced across the board. Rates vary between USD900 - 1250 per TEU.

- The most competitively priced are options with Cosco into the East Coast & West Coast.

- Rate levels into the West Coast (FRE/ADL) vary between USD1250 - 1450 per TEU.

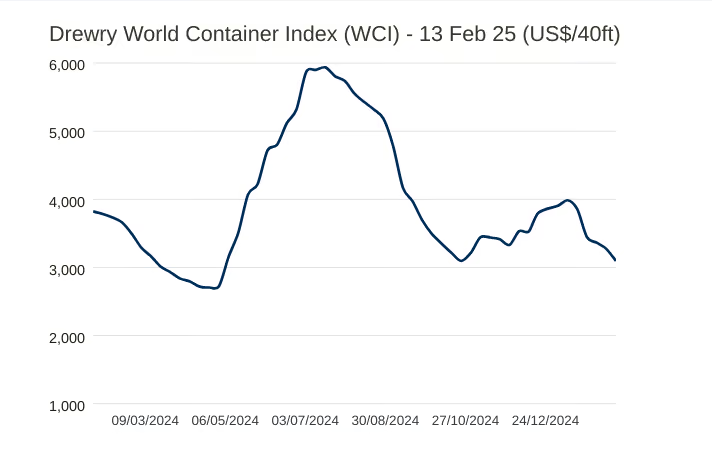

- The Drewry WCI composite index decreased 5% to $3,095 per 40ft container, 70% below the previous pandemic peak of $10,377 in September 2021. However, the index was 118% higher than the average $1,420 in 2019 (pre-pandemic).

Capacity and schedule reliability

Capacity

- Carriers have open capacity after the Chinese New Year, with the market in somewhat of a lull.

- Shipments that were booked ahead of the New Year experienced congestion and delays due to a surge in demand. Normal operations have mostly resumed, with carrier roll pools beginning to clear.

- For urgent orders, it is recommended that bookings are made on the A3 service. Cosco/OOCL have a reduced risk of rolling.

- Without a change in demand, we can expect blank sailings to commence in late March/early April to restore balance to the market.

- Space out of Southeast Asia is also readily available.

Schedule reliability

- Intermittent strikes in Chittagong have resulted in a backlog of containers that could take up to 2 weeks to clear. There are currently 16 vessels at anchor awaiting a berth. This could be problematic leading up to Ramadan. Ramadan typically results in a countrywide reduction in working hours that transpires until after Eid, which concludes on March 30. Source: Yahoo

- Congestion remains in Singapore, with an average wait time of 3 days to berth.

- Shanghai also has some congestion, with 163 vessels scheduled to arrive before the end of the month. Dalian and Ningbo are also seeing mild congestion and vessel waiting times.

North America

North America

Ocean rates

- TPEB pricing has declined during February with rates anticipated to continue their downward trajectory into March.

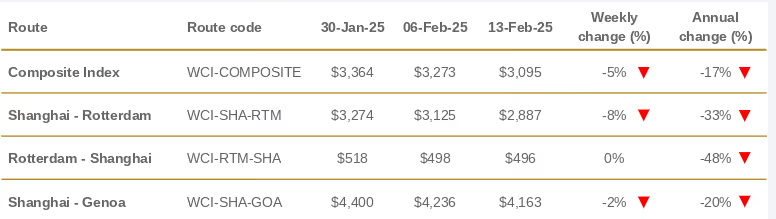

- Shanghai to Los Angeles fell 7% or $325 to $4,392 per 40ft container. Los Angeles to Shanghai decreased 1% to $703 per 40ft container. Source: Drewry

- TAWB pricing remains stable, with levels sitting at approximately USD1000-1200 per TEU.

Capacity

- December and early January were the busiest on record for US imports in many years. The frontloading and rush pre-CNY exceeded even COVID levels in terms of overall volume.

- Severe weather in the USA and Canada will disrupt transportation across both nations. The Polar Vortex disruptions aloft have established extreme weather conditions, with long-lasting Arctic cold outbreaks and intense winter storms this month. On Sunday, a Winter Storm Jett will blast part of the Great Lakes and Northeast U.S. with intense snowfall, freezing rain, and snow blizzards. Then, another significant Arctic cold outbreak follows next week. The frigid cold air mass has maintained over much of Canada and the northern U.S. over the last two weeks and is forecast to plunge far south across the nation in the coming days. Temperatures are forecast to push back into a deep freeze, with 40 to more than 50 degrees F below normal for tens of millions across the North American continent. Source: Severe Weather Europe

Schedule reliability

- Marine terminals at the Port of New York and New Jersey are seeing bouts of severe congestion due to heavy import volumes, holiday scheduling, and bad weather. Between Week 7-9, there is an expected approx. 17,000 TEUs of empty equipment to be evacuated from the terminals. Subsequently, an average of 2,500 TEUs will be evacuated thereafter. Source: JOC / Hapag Lloyd

- Rail terminals currently have a shortage of 20’ equipment. This will attract additional surcharges.

US Tariffs

- President Trump temporarily reversed his decision to suspend the de minimis provision, citing that the CBP (Customs & Border Protection Agency) did not have sufficient systems in place to handle such a large influx of shipments requiring more complex import clearances. There has been a 30-day ‘pause’ on the suspension, however, it is likely to take much longer to implement systems to accommodate such a significant change. CBP simply wasn’t able to handle the volume of parcels that piled up rapidly. By the time the US government suspended the measure, more than a million were sitting at New York’s JFK airport alone waiting to be processed.

- President Donald Trump said he is planning to enact automotive tariffs “around April 2,” in response to a reporter’s question on Friday. Trump did not expand on which countries would be impacted nor how much the tariffs would be. Earlier this month, Trump signed an executive order to enact 25% tariffs on foreign steel and aluminum imports. While the impacts will differ by company, many automakers rely on imported steel and aluminum materials. Meanwhile, the president ordered a 25% tariff on all imports from Mexico and Canada. While the tariffs were meant to go into effect Feb. 4, the U.S. decided to delay implementation until March 4 for both Canada and Mexico. The move against the U.S.’s two largest trading partners would further “blow a hole” in the U.S. auto industry, Ford Motor Co. CEO Jim Farley said during a recent investor conference. Source: Supply Chain Dive

Europe

Europe

.png)

Ocean freight rates

- FEWB rates again took a dive, despite carriers efforts to control the market via blank sailings and advertised GRIs in March.

- Spot rates ex Northeast Asia to Europe are sitting at approximately USD1100-1400 per TEU in the second half of Feb.

- Freight rates from Shanghai to Rotterdam decreased 8% or $238 to $2,887 per 40ft container, with those from Shanghai to Genoa decreased 2% to $4,163 per 40ft container. Source: Drewry

Capacity and schedule reliability

Capacity

- The overall market has been slack post Chinese New Year in the FEWB trade. There is an oversupply of capacity, with blank sailing a possibility.

- TAWB trade has experienced steady demand this month, with rate restorations on the cards for March. The EU-US trade war is intensifying which could have a big impact on this trade passage.

Schedule reliability

- Ongoing congestion plagues the port of Rotterdam due to unplanned industrial action by the workers represented by the FNV Havens and CNV unions. Terminals are currently full and unable to take on more containers until the backlog is cleared. There is currently congestion of 76 hours at Rotterdam and delays at Antwerp of 70 hours. Source: The Loadstar

- Port strikes in France have resulted in congestion across terminals. Four-hour stoppages took place on February 10, 12, and 14. Additional four-hour stoppages are planned for February 18 and 19.

- Due to the ongoing congestion in Rotterdam, Le Havre, and Hamburg, the Port of Antwerp is now being used as an alternative. Carriers (OOCL/Hapag Lloyd) are reporting high yard utilisation levels and operational delays. DP World has also announced a critical situation of yard occupancy.

- Vessels are not likely to return to the Suez Canal until the end of Q1/early Q2. Extended routings via the Cape of Good Hope will be in place for the foreseeable future. This mostly impacts shipments on the FEWB and TAWB trades.

Global air freight

- The market is heating up now that factories are resuming work after the Chinese New Year. There has been an influx of e-commerce volume to the market and rates will begin to increase after a few weeks of very competitive levels.

- PVG services are starting to hit capacity with some airlines. HO (Juneyao Air) is fully booked to SYD/MEL until the end of the month. NH (All Nippon) is also fully booked into SYD.

- Space with MU (China Eastern) into SYD/BNE is becoming very tight, with standby flights likely.

- WorldACD has reported that its latest data showed tonnages from China to the US dropped steeply in week 5 (27 January-2 February) and week 6 (3-9 February).

- But there were similar WoW declines in tonnages from China to Europe of -30% in week 5 and a further -20% in week 6, with Hong Kong to Europe tonnages holding up little better (-22%, and a further -17%, WoW, respectively).

- However, spot rates from China to Europe were relatively stable, dipping -2% in week 5 and a further -4% in week 6, to $3.91 per kilo – almost exactly their level in week 6 last year.

- Spot rates from China to the US, meanwhile, dropped by -7%, WoW, in week 5, and a further -3% in week 6, to $3.99 a kilo, taking them -19% lower year on year, with Hong Kong to US rates 14% down year on year.

- Air cargo tonnages to the US from other East Asian countries that celebrate LNY also declined sharply in week 5, WoW, including South Korea (-42%), Taiwan (-60%) and Vietnam (-58%), although volumes rebounded or partially rebounded in week 6, with a +21% WoW recovery in South Korea, +68% rebound in Taiwan, and a +31% partial bounce-back in Vietnam. Source: Air Cargo News

- Schiphol Airport’s proposed new tariffs – a 41% hike from 1 April, are set to impact inbound freight. The proposed tariff hikes, under consideration by the ACM after complaints, are substantial: an average of 37% over three years. And 2026 will see a further 7.3% rise, and then 12.5% from April 2027. Schiphol has argued that it needs the money for nvestments in airport infrastructure and process efficiencies. Source: The Loadstar

General news

- MSC cargo ship runs aground in Newfoundland. The MSC Baltic III was about 12 nautical miles outside of the entrance to Bay of Islands when it reported losing power. All 20 people on board the ship were safely airlifted from the vessel Saturday morning by a Cormorant helicopter. Source: Global News

- The Australian Department of Agriculture, Fisheries, and Forestry have tightened controls on import goods out of Germany. On 10 January 2025, Germany provided official notification to the World Organisation for Animal Health (WOAH) of the detection of foot-and-mouth disease (FMD) in a herd of water buffalo in the eastern state of Brandenburg. This is the first detection of FMD in Germany since 1988. Products under scrutiny include meat, dairy, pet foods, veterinary therapeutics, animal feed, and reproductive materials. Source: DAFF

- East Pilbara Shire in Western Australia’s northwest has been one of the worst hit in the aftermath of Tropical Cyclone Zelia’s coastal crossing with roads cut and communities isolated. Freight routes across the remote Pilbara region are set to be cut for days, sparking panic buying with supermarket shelves stripped bare at Broome.

- However, authorities said contingencies were in place to have trucks arrive via South Australia and the Northern Territory to help restock stores. Former category five system Zelia was quickly downgraded to a tropical low once it crossed the coast. Source: The Nightly

- Maritime Union welcomes WA Labor Government’s Investment in Supply Chain Resilience. The Labor Government is to establish a $5 million Supply Chain Resilience Fund aimed at bolstering Western Australia’s shipping capability. The MUA has long advocated for the reinstatement of a dedicated WA coastal shipping service to ensure essential supplies reach communities during times of crisis and to strengthen local employment opportunities for Australian seafarers.MUA WA Branch Secretary Will Tracey said the announcement was a positive step towards reintroducing a dedicated shipping service to the WA coast. Source: MUA

Interesting Articles

.avif)

Brad Turnbull

Head of Pricing & Procurement

Experienced Business Development Manager with a demonstrated history of working in the logistics and supply chain industry. Skilled in Import/Export, Freight Transportation, Freight, Warehouse Operations, and Overseas Networking.

References

Frequently Asked Questions

Explorate gives supply chain managers one real-time view across ever forwarder, lane and mode without replacing your current process, partners or systems.

What is Explorate and what services does it provide?

How is Explorate different from a traditional freight forwarder?

Why does Explorate provide these Market Updates?

How can I use the data in these updates to optimise my supply chain?

Where does Explorate source the intelligence for these reports?

Can I request my own quote?