.avif)

Australia

Australia

- Hutchinson Ports (SYD): MUA - STOP WORK MEETING will be held on May 1st from 10:00 to 14:00.

Port Delays.

- Sydney Port is currently facing congestion following a period of severe weather that has caused ongoing delays. Terminal operations have been disrupted by thunderstorms, hail, and damaging winds, leading to a backlog in vessel schedules and reduced port productivity.

North East Asia

North East Asia

- As China’s Labour Day Golden Week holiday approaches, manufacturing operations across the country are expected to pause for 5 to 7 days, with factory closures likely impacting cargo availability between May 6 and 14. In response, carriers have implemented sailing cancellations and service adjustments, but capacity pressure remains high as lines work to fill vessels post-holiday.

- Looking ahead, shipping lines remain optimistic for post-holiday demand recovery. A General Rate Increase (GRI) of USD 300/600 per 20GP/40HC has been announced, with carriers hoping to increase rates to levels in excess of USD1150 per TEU. However, achieving this could prove difficult. May is traditionally a low-demand month, and unless carriers implement significant blank sailings in the second half of May, rates are more likely to stabilize at a moderate level closer to USD950 per TEU.

- Despite short-term disruptions, cargo volumes remain strong, showing year-on-year growth compared to May 2023, and even slight gains over May 2024 levels—indicating continued resilience in the market.

- With scattered blank sailings in May, space remains stable, and rates are following suit.

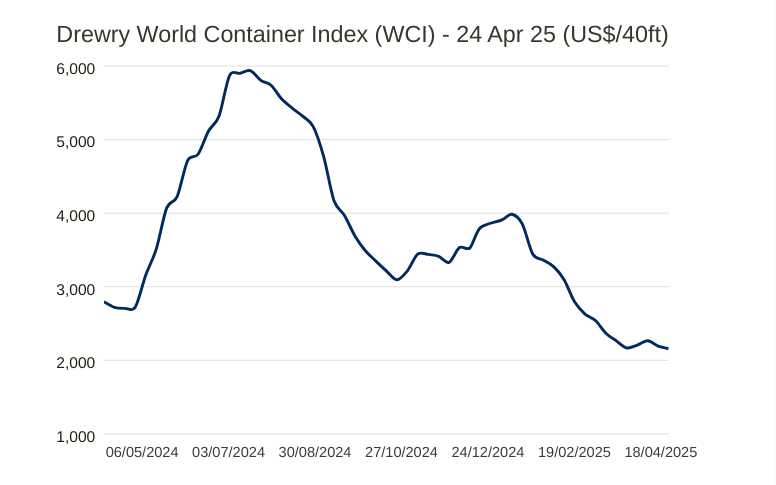

- The Drewry WCI composite index decreased by 2%, reaching $2,157 per 40ft container. This is 79% lower than the pandemic peak of $10,377 in September 2021 but still 52% higher than the pre-pandemic average of $1,420 in 2019.

- The average year-to-date (YTD) composite index closed at $2,854 per 40ft container, which is $38 lower than the 10-year average of $2,891, impacted by the exceptionally high rates during the 2020-2022 Covid period.

Ocean freight rates

- Several major carriers operating CAT and CA2 services—including TSL, PIL, YML, and SNL—have implemented notable rate reductions across key lanes. These adjustments, first applied to South China origins (Shenzhen) in late April, were subsequently extended to East China (Shanghai, Ningbo) and North China (Qingdao) through early May. These moves reflect a strategic response to softening demand during the Golden Week holiday period, with reductions averaging 15–20% compared to early April levels.

- NEAX (A1X), operated by HMM, EMC, ONE, and HPL, while not a premium service, has maintained competitive positioning. These carriers have introduced modest downward adjustments, aligning their offers slightly above the most aggressive market rates, indicating a 10–15% decrease to remain within reach of the lowest-priced offerings.

- The ZAX (PANDA) service, jointly operated by MSC and ZIM, has responded aggressively to market pressure by aligning closely with the lower-tier rates on lanes from Shenzhen, Ningbo, Shanghai, and Qingdao to Australia’s East Coast (AUEC) hubs. From Tianjin, ZIM has also introduced compelling adjustments, reflecting an average 10–15% decrease from previous benchmarks.

- On the premium services—including A3S, A3C, A3N, JKN, and CNS—operated by COSCO, ANL, and OOCL, carriers have proactively narrowed the gap with mid-range offerings. Rate adjustments across all major Chinese ports reflect a 10% reduction, showing a tactical effort to remain competitive while maintaining service differentiation.

- For Fremantle and Adelaide (FRE/ADL), rates have largely remained stable due to already being at relatively low levels. No significant changes were observed during the current period.

- LCL pricing offers competitive options for May with minimal disruption overall.

Capacity and schedule reliability

Capacity

- Due to tariff changes affecting the U.S. market, some vessels with larger loading capacities have been redirected from the U.S. trade lane to the Australian route. MSC is gradually replacing vessels on this route with larger ships (8,000+ TEU capacity).

- In early May, TSL added an extra loader vessel, TS MELBOURNE 2502S, to accommodate schedule delays. As a result, vessels operating on the CA2 service will now be departing around the same time in mid-May.

- Additionally, MSC's WALLABY service has stopped accepting bookings from New Zealand as of April 25, which has increased space availability for shipments to Australia. Please note that this service only calls at Sydney and Melbourne ports.

- Given these developments, there is currently sufficient shipping space available for May, contributing to recent freight rate reductions.

Schedule reliability

- Qingdao: Port reliability has seen a direct operational improvement following a period of intermittent weather disruptions. The active anchorage queue dropped substantially down to 28 vessels waiting to berth this week, a sharp reduction from the 57 vessels reported stranded in the previous update.

- Tianjin: Localized bottleneck pressures and congestion backlogs have significantly cleared out. Only 3 vessels were left sitting at anchor this week, comparing favorably to the 15 vessels stuck waiting during the prior tracking cycle.

- Holiday Disruption Adjustments (Labor Day Golden Week): With China's multi-day factory closures approaching, manufacturing output is slated to pause for 5 to 7 days, impacting localized cargo availability directly between May 6 and May 14. In anticipation of this drop, ocean carriers have preemptively rolled out widespread sailing cancellations and last-minute service rotation adjustments to re-stabilize and artificially preserve their forward schedule integrity.

- Container Equipment Availability: Across primary North East Asian origin load gates, empty container equipment inventories remain fundamentally healthy and stable. No systemic or widespread equipment deficits are actively harming localized schedule originations.

South East Asia

South East Asia

.avif)

Ocean freight rates

- Rates out of Southeast Asia have shifted slightly by only 5% with certain carriers.

- There is a large difference of rates between carriers, with a variance of approximately 30% between the lower and higher end of the market.

Capacity and schedule reliability

Capacity

- Subdued Volume Growth: Export volume growth running from South East Asia toward North America remains completely flat and subdued. Total container throughput for the month of April held steady at approximately 6,000 TEUs, showing no growth or variation from the identical baselines tracked month-on-month between January and March.

- Open Ocean Space: On the Southbound Oceania lane, carriers are reporting wide open and available physical space. Shippers are facing no direct structural slot shortages on vessel hulls, though the actual movement of this capacity is restricted by congestion bottlenecks tying up transhipment hubs downstream.

- GRI Dependency: Carriers have queued up an early-May General Rate Increase (GRI) for Transpacific Eastbound (TPEB) routes, but lines have explicitly stated that the success and deployment of these capacity rate hikes are entirely tethered to cargo flow out of South East Asia. Because regional volumes have remained soft, carriers are taking a "wait and see" approach, indicating that if South East Asian volumes do not pick up, the planned GRI will be delayed or scaled back.

Schedule reliability

- Port Klang (Malaysia): The port is dealing with a notable structural backlog, forcing arriving vessels into berth waiting times of up to 3 days.

- Yard Congestion Metrics: Local yard density has broken past critical operational thresholds to sit over 80% capacity, which is actively dragging down terminal handling speed and overall port productivity.

- Anchorage Volume Tracking: The offshore pipeline remains heavily bottlenecked, with exactly 22 vessels stranded at anchor waiting for a designated berth slot to clear.

North America

North America

Ocean rates

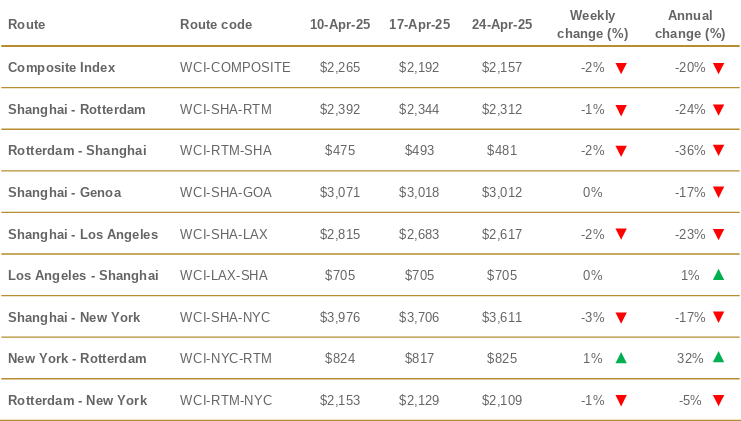

- Shanghai to New York: 3% decrease, now at $3,611 per 40ft container.

Shanghai to Los Angeles: 2% decrease, now at $2,617 per 40ft container. - Rotterdam to New York: 1% decrease, now at $2,109 per 40ft container.

- Rates from Shanghai to Genoa and Los Angeles to Shanghai remained stable.

- Carriers have announced a General Rate Increase (GRI) targeting early May for TPEB routes. However, the success of these rate hikes appears tied to cargo flow out of Southeast Asia. If volumes stay soft, as they have been recently, the GRI may either be delayed or scaled back.

- Several carriers are also lining up Peak Season Surcharges (PSS) for the second half of May. Yet again, the actual implementation will likely depend on how the market responds to the early-May GRI efforts. Carriers seem to be taking a "wait and see" approach, adjusting strategies based on demand signals over the coming weeks.

- There is available space on the Southbound Oceania lane, although some routes are experiencing congestion at transshipment ports.

-

Capacity

- Shipping volumes from China to North America are experiencing a sharp decline, with around 50% of scheduled shipments being canceled. Meanwhile, volume growth from Southeast Asia to North America remains subdued, with April’s throughput holding steady at approximately 6,000 TEUs — similar to the levels seen from January through March.

- Ocean carriers are cutting capacity on the Transpacific Eastbound trade aggressively. In response to the anticipated drop in demand following the latest U.S. tariffs on Chinese goods, carriers are scaling down operations by deploying smaller vessels, canceling scheduled sailings, and even suspending entire service loops.

- Major shipping alliances — including Ocean Alliance (CMA CGM, COSCO, Evergreen, and OOCL), Premier Alliance (ONE, HMM, YML), and the ZIM/MSC partnership — have suspended eight weekly services in total. Additionally, blank sailings have been increasing across other carriers and alliances, with further cancellations likely as market conditions evolve.

- Between late April and early May, over 25% of weekly service loops have already been canceled — a figure that even exceeds the levels during COVID.

Schedule Reliability

Overall, container availability at major Asian origin ports for Transpacific Eastbound (TPEB) shipments remains healthy. That said, pockets of equipment shortages are being reported at certain Southeast Asian ports. While these shortages aren’t causing widespread disruptions, shippers with cargo originating from those locations should stay alert and plan accordingly.

US Tariffs

Key updates (as at 30 April 2025):

- Significant Decline in China-U.S. Trade Volumes: Kuehne + Nagel CEO Stefan Paul reported a substantial drop in volumes and bookings on the China-U.S. tradelane, attributing this to the hefty import tariffs imposed by the Trump administration. Source: The Loadstar

- Complete Halt in Certain Supply Chain Activities: The tariffs have led to a complete stop in some supply chain activities, indicating a severe disruption in trade flows between China and the U.S.

- Variability Across Different Sectors: The impact of the tariffs varies across different industry verticals, with some sectors experiencing more pronounced effects than others.

- Contrasting Effects on Sea and Air Freight: There is a contrasting picture between sea and air freight, suggesting that the mode of transportation influences how the tariffs affect logistics operations.

- Strategic Reassessment by Logistics Providers: The current trade environment is prompting logistics companies like Kuehne + Nagel to reassess their strategies and operations to navigate the challenges posed by the new tariffs.

Blank sailings surge.

- Transpacific container shipping is experiencing a significant surge in blank sailings, primarily due to the ongoing U.S. tariff war. According to Sea-Intelligence, the Asia–North America East Coast route saw blanked capacity rise from 35% to 42% for the week starting May 5, 2025. Similarly, the West Coast route's blanked capacity increased from 13% to 28% for the week beginning April 28. These levels are typically observed during seasonal slowdowns like Chinese New Year or Golden Week, but the current spike is attributed to sudden demand drops and limited advance notice to shippers. The escalation in blank sailings reflects carriers' responses to reduced demand, as shippers pause or cancel shipments amid tariff uncertainties. This abrupt capacity reduction poses challenges for supply chain planning, with many cancellations announced on short notice. The situation underscores the volatility in the market and the need for shippers to stay informed about schedule changes. Source: Sea Intelligence

👉 Read the full update in our Dedicated Tariffs Blog.

Europe

Europe

.png)

Ocean freight rates

- Rotterdam to Shanghai: 2% decrease, now at $481 per 40ft container.

- Rotterdam to New York: 1% decrease, now at $2,109 per 40ft container.

- New York to Rotterdam: increased by 1% to $825 per 40ft container.

- Shanghai to Rotterdam: 1% decrease, now at $2,312 per 40ft container.

We can expect rates from Europe to Oceania to remain stable into quarter 2.

Capacity and schedule reliability

Capacity

- Space on direct services with CMA CGM and MSC remains constrained due to high demand. Meanwhile, backlogs on relay services via Singapore and Port Klang have largely been resolved. However, some schedule disruptions persist — notably, the direct service has chosen to omit Rotterdam on seven consecutive sailings, citing ongoing delays and congestion. Antwerp has been designated as the alternative port of call for these voyages.

- In the first quarter of 2025, the Port of Antwerp-Bruges surpassed Rotterdam to become Europe’s busiest container port, handling 3.43 million TEUs compared to Rotterdam’s 3.36 million TEUs. Source: JOC

Key Highlights

- Increased Throughput: Antwerp-Bruges experienced a 6% year-over-year increase in container volumes during the first quarter.

- Strategic Investments: The port has invested in infrastructure and digitalization to enhance efficiency and attract more shipping lines.

- Market Dynamics: The shift in rankings reflects changing global trade patterns and the strategic positioning of European ports.

Schedule reliability

🇬🇧 United Kingdom

London Gateway Port:

- High yard utilization and a full berthing lineup, challenging productivity.

- Delays to trucking and rail are expected post-Easter.

Southampton:

- 7-day average vessel waiting time: 2.40 days.

- Operating at 90% utilization, with reefers at 70%.

- Increased pickup demand expected to cause potential landside delays after Easter.

🇧🇪 Belgium

Antwerp:

- High yard congestion, especially at DP World Antwerp Gateway 1700. Stacking capacity is fully utilized, and export truck slots have been reduced by 30% to prioritize import container clearance.

- Yard utilization >92% and frequent vessel calls are causing delays, compounded by strikes, vessel phase-in/out schedules, and low water levels on inland routes.

- Labor availability is lower due to recent holidays.

- Terminals are adjusting priorities to clear export and transshipment containers. Some terminals are rejecting additional import or transshipment cargo.

- To ease congestion, no empty containers are accepted, and export delivery windows have been shortened from 7 to 5 days. Disruptions expected until late April.

🇩🇪 Germany

Bremerhaven:

The terminal anticipates post-Easter challenges due to labor shortages, potentially causing delays in the vessel lineup.

Hamburg:

- On 17 March, HHLA imposed delivery restrictions to manage yard congestion. Berthing lineups remain full, and delays to pickups and deliveries are expected after Easter.

- Rail processing at CTB is delayed by 10 hours.

- Full rail closure from 4-8 July, halting rail transport to/from Hamburg.

🇫🇷 France

Le Havre:

Crane maintenance at CNMP has been completed, and the terminal is back to full operational capacity, improving productivity.

🇳🇱 Netherlands

Rotterdam:

- Increased yard density due to labor shortages during the spring holiday period .

- Most terminals operated waterside only during Easter.

- Congestion expected for pickup and delivery, with feeder delays of 2-6 days.

🇬🇷 Greece

Piraeus:

Average vessel waiting time of 3.79 days due to congestion.

Global air freight

Asia Pacific

Tonnage: Decreased by 4% week-on-week (WoW).

Rates: Fell by 3% WoW; spot rates dropped 6%.

China & Hong Kong to USA: Traffic declined for the fourth consecutive week, down 7% WoW and 16% year-on-year (YoY).

Emerging Markets: Exports to the USA from Vietnam (+42%), Taiwan (+30%), Thailand (+24%), and Japan (+12%) showed strong YoY growth.

Australian Imports: Space to SYD and MEL remains tight ex Southern China. Rates are stable across the main hubs, with congestion expected on secondary legs. Suggest to book in advance.

Europe

Rates: Spot rates decreased by 6% WoW.

Tonnage: Experienced a WoW decline, contributing to the global downturn.

Africa

Tonnage: Saw a significant WoW increase of 15%.

Rates: Spot rates declined by 6% WoW.

Central & South America

Tonnage: Increased by 3% WoW.

Rates: Remained stable, with no significant WoW changes.

Middle East & South Asia (MESA)

Rates: Experienced a 4% WoW decline; spot rates decreased by 6%.

YoY Comparison: Rates are down approximately 16% compared to the same week last year.

North America

Tonnage: Declined by 2% WoW.

Rates: Increased by 4% WoW, the only region to register a rate increase.

Global Overview

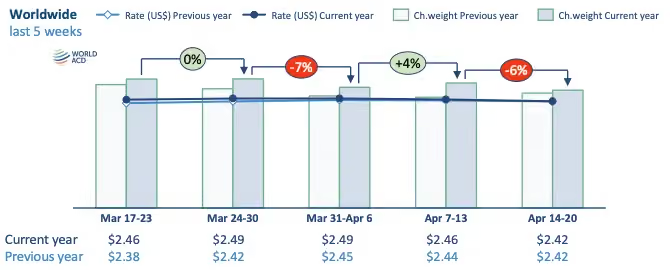

Tonnage: Overall worldwide chargeable weight dropped by 6% WoW.

Rates: Average global prices decreased by 2% to US$2.42 per kilo; spot rates fell by 4% to $2.58.

YoY Comparison: Global rates are similar to the same week last year, except for MESA, which is down by around 16%. Source: World ACD

Mumbai International Airport (MIAL), a critical hub for India's air cargo, is set to undergo significant infrastructure upgrades starting in August 2025. The $1 billion project, led by Adani Airport Holding, will involve the closure of freighter slots for several months to facilitate the construction of new taxiways and other enhancements aimed at increasing operational efficiency. Source: JOC

Key Implications:

- Disruption to Air Cargo Operations: The closure of freighter slots is expected to disrupt air cargo operations, particularly affecting the movement of goods through one of India's busiest freight corridors.

- Impact on Supply Chains: Businesses relying on timely air freight services may face delays, potentially affecting inventory management and delivery schedules.

- Strategic Planning Required: Shippers and logistics providers will need to adjust their strategies, possibly by seeking alternative routes or modes of transport, to mitigate the impact of the upcoming disruptions.

General news

- A massive explosion at Iran's Shahid Rajaee Port in Bandar Abbas on April 26, 2025, killed at least 70 people and injured over 1,200. The blast caused significant damage, including collapsed buildings and large craters. While the exact cause remains unclear, reports suggest that improperly declared hazardous cargo, including ammonium perchlorate (a chemical used in missile fuel), may have triggered the explosion. The incident has raised concerns about port safety and regulatory oversight in Iran, especially given the possible involvement of high-level figures bypassing customs procedures. Iran's Supreme Leader has ordered an investigation into the incident, and the fire at the port was extinguished after two days, though flare-ups continue. Source: Container News

- China Eastern Air Logistics has launched a new South Australia product portfolio, unveiled at Adelaide's Ayers House on April 11, 2025. This initiative includes a procurement memorandum of understanding between China Eastern Airlines Cold Chain and Ferguson Australia, aiming to enhance the import of premium Australian goods such as salmon, wine, Manuka honey, and chilled steaks into China. Leveraging China Eastern Airlines' extensive aviation network, the logistics unit can distribute these products to 80% of China's consumers within 12 hours post-customs clearance. The company is also developing processing facilities in cities like Chengdu, Ningbo, and Ezhou to expedite delivery times further. Additionally, a co-branded product line, "South Australia Premium Selection, China Eastern Airlines Logistics Fresh Delivery," in partnership with Ferguson Australia and Penfolds Winery, is set to debut in the Chinese market. Source: Asian Aviation

- The Maritime Union of Australia (MUA) has strongly criticized DP World's plan to automate container terminals in Melbourne, Sydney, and Brisbane, warning that the move will reduce productivity, increase costs, and compromise safety. The union alleges that DP World, which controls about one-third of Australia's port infrastructure, intends to invest over $600 million to replace skilled Australian dockworkers with automated equipment, without adhering to consultation requirements outlined in their Enterprise Agreement. The MUA contends that automation is not a viable solution for enhancing port productivity, citing international examples where automated terminals have proven to be slower, more expensive, and less safe compared to those operated by human workers. Additionally, the union raises concerns about the reliability of automated systems, which can be adversely affected by environmental factors and are susceptible to cyberattacks, referencing a 2023 incident where Russian hackers disrupted DP World's port operations in Australia. The MUA urges DP World to reconsider its automation plans and instead focus on collaborative approaches that prioritize the interests of workers and the broader community. Maritime Union of Australia

Interesting Articles

.avif)

Experienced Business Development Manager with a demonstrated history of working in the logistics and supply chain industry. Skilled in Import/Export, Freight Transportation, Freight, Warehouse Operations, and Overseas Networking.

Frequently Asked Questions

Explorate gives supply chain managers one real-time view across ever forwarder, lane and mode without replacing your current process, partners or systems.