.avif)

Australia

Australia

Patrick Stevedore 2026 Enterprise Agreement

- Historic Agreement Reached Early:

Reached eight months ahead of the 2022 agreement’s expiry, with near-unanimous national support from members across Patrick’s four container terminals. - Symbolic Timing:

Finalised during the 27th anniversary of the 1998 Waterfront Dispute, marking a significant and peaceful milestone in union-company relations. - Major Wins for Workers:

- $2,000 sign-on bonus upon Fair Work Commission registration.

- Annual pay increases through to 2028, based on the greater of CPI or:

- 3.25% in Jan 2026 & 2027

- 3.5% in Jan 2028

- Superannuation increase to 12.5% from July 2025 (0.5% above SGC).

- Protect Income Protection increase to 2.25%.

- Expanded personal leave payouts on termination.

- Guarantees of No Forced Redundancies (including automation) and No Outsourcing.

- Cooperative Negotiations:

Talks began in late 2024 with a shared aim to avoid lengthy disputes. The deal was reached without industrial action - a first since 1998. - Fair Work Registration Pending:

Agreement and associated declarations are being prepared for submission to the Fair Work Commission. - Union Perspective:

MUA highlights this as a model of what’s possible when both sides engage in genuine, good-faith negotiations, offering stability amid global uncertainty. Source: MUA

Port Delays

- DP World:

- Sydney: 4 day waiting time

- Brisbane: 1-4 day waiting time

- Melbourne: 1 day waiting time

- Patrick Terminals

- Sydney: A crane malfunction incident between April 5-7 led to delays of approximately 2 days. Current berth waiting time is 4 days.

- Brisbane: 0.5 day waiting time

- Melbourne: No delays

- Hutchison:

- Brisbane: 1-5 day waiting time

- Sydney: No delays

- VICT

- Melbourne:1 day waiting time

North East Asia

North East Asia

- Over the past several weeks, we’ve seen all major shipping lines attempt to implement General Rate Increases (GRIs) of USD 300/TEU on a biweekly basis. It’s clear: carriers are eager to see freight rates climb -and they’re taking action to make that happen.

- Starting in mid-March, blank sailings became a common tactic to tighten supply and support higher rates. That said, not all carriers are following the same playbook. Some carriers have upgraded their vessels, while others are working together more strategically, continuing to pull sailings to carefully manage the supply/demand balance.

- As we move through the traditionally quiet season of March–April, carriers appear to be succeeding in holding rate levels steady while nudging them up incrementally. Long-term NAC contracts are holding firm with carriers determined not to let spot rates dip below key support levels -especially with BCOs and forwarders watching the market closely.

- Overall, the spot rates have remained stable moving into the second half of April, with very minimal change.

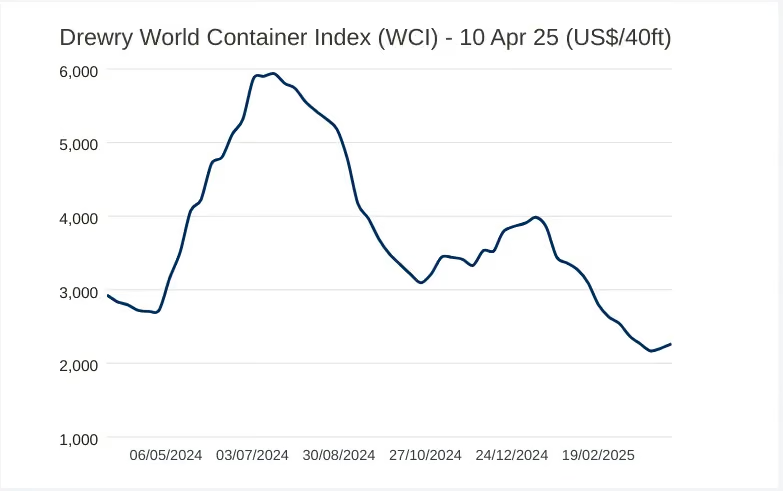

- The Drewry World Container Index (WCI) rose by 3% this week, reaching $2,265 per 40ft container. While that’s still a 78% drop from the pandemic peak of $10,377 in September 2021, it's 59% higher than the pre-COVID average of $1,420 in 2019 - showing how rates remain elevated compared to historical norms.

- So far this year, the average year-to-date WCI sits at $2,944, which is $55 above the 10-year average of $2,889 - a figure heavily influenced by the rate surges seen during 2020–2022. Source: Drewry

Ocean freight rates

- OOCL: USD 300.00 per TEU for all cargo ex Northeast Asia to Australia.

- ANL: USD 300.00 per TEU for all cargo ex Northeast Asia to Australia.

- MSC: USD 300.00 per TEU for all cargo ex China, Hong Kong, Japan, Korea, and Taiwan to Australia and New Zealand.

- U.S. West Coast routes (Platts): Dropped by $900 down to USD 1,600 per FEU (a 36% weekly decline).

- U.S. East Coast routes (Platts): Dropped by $500 down to USD 3,000 per FEU.

Capacity and schedule reliability

Capacity

- The CAE service is blanking in Week 18.

- The CAT service is blanking in Week 19.

- The A3 service is blanking in Week 17.

- The ZAX service is blanking in Week 17.

- Tianjin (22/Apr) → Qingdao (23/Apr) → Shanghai (24/Apr) → Ningbo (25/Apr) → Shekou (27/Apr) → Nansha (28/Apr) → Brisbane (10/May) → Sydney (13/May) → Melbourne (16/May).

Schedule reliability

Pre-Holiday Sailing Integrity: Schedule reliability across North East Asian loading gates is holding steady, but the upcoming holiday blanking schedules (Weeks 17 to 19) are expected to cause brief operational delays and container roll pools at origin ports as carriers alter standard service rotations.

South East Asia

South East Asia

.avif)

Ocean freight rates

Capacity and schedule reliability

Capacity

Schedule reliability

Hub Delays: Vessel schedules are tracking unevenly due to the combination of container equipment deficits and the sudden influx of overbooked cargo rushing to catch U.S. connections. This space battle is causing minor container tracking delays and routing re-assignments across primary transhipment networks.

North America

North America

Ocean rates

- Shanghai to Los Angeles: Increased by 3% (up $89) to $2,815 per 40ft container.

- Shanghai to New York: Rose by 2% to $3,976 per 40ft container.

- Los Angeles to Shanghai: Remained stable.

- New York to Rotterdam: Decreased by 1% (down $7) to $824 per 40ft container.

- Rotterdam to New York: Increased by 1% to $2,153 per 40ft container.

These adjustments reflect a tightening of capacity and the early impacts of recent tariff changes. Drewry anticipates further rate increases in the coming weeks due to ongoing capacity reductions and tariff pressures. Source: Drewry

- As a result of reduced volumes and softening demand, freight rates from North Asia to North America dropped sharply.

- Platts Reported Rates (North Asia → U.S. West Coast) fell by $900 to $1,600/FEU, a 36% weekly decline.

- While, (North Asia → U.S. East Coast) dropped $500 to $3,000/FEU. Source: S&P Global

Capacity

- The Port of Los Angeles experienced a 1.6% increase in imports in March 2025, totaling 385,531 TEUs. However, Executive Director Gene Seroka has cautioned the industry to "buckle up," anticipating a significant downturn due to escalating trade tensions with China. The port is preparing for a potential 10% decline in cargo volumes starting in May, driven by reduced orders from retailers and manufacturers responding to rising tariffs on Chinese imports. Source: WorldCargoNews

- Uncertainty surrounding ongoing tariff negotiations between the US and China kept participants in the North American container freight market cautious. Amid shifting trade dynamics, many shippers chose to delay new bookings or cancel existing ones while awaiting greater clarity.

- There have been several last minute cancelations for container bookings ex China to the USA, with several others rushed ahead of the new tariffs on April 9. This trend is expected to continue through May, potentially driving a spike in fronthaul volumes from non-China Asian origins. The U.S. 90-day pause on tariffs above 10% is encouraging shippers to move quickly before further increases.

- Given the current state of global trade, many shipping lines have been compelled to scale back their services to the US. As a result, a surplus of vessels are now being redirected to alternative trade routes. This shift is expected to impact both space availability and freight rates across other lanes.

- Trans-Pacific Eastbound carriers are expected to announce additional blank sailings following a wave of booking cancellations last week, which may result in vessels departing China with significantly reduced loads through May.

- With ongoing uncertainty surrounding the implementation of new U.S. tariffs on Chinese goods, many shippers are being forced to make last-minute decisions regarding their now costlier shipments. Port of Los Angeles Executive Director Gene Seroka confirmed that 12 sailings from China to the U.S. West Coast scheduled for May have already been canceled in response to the recently announced 145% tariff on a wide range of Chinese imports. Source: JOC

Schedule Reliability

🇨🇦 Canada – Rail & Port Congestion Update

Vessel Wait Times & Rail Dwell (Import Cargo – Vessel Arrival to Rail Departure):

- Halifax: 8 days

- Montreal: 10 days

- Prince Rupert: 13 days

- Saint John: 7 days

- Vancouver: 13 days

Vancouver:

Average vessel waiting times have climbed to approximately 7.5 days this week amid ongoing port congestion. Prolonged rail container dwell times persist due to lingering winter weather challenges and a backlog caused by longshore labour disruptions in late 2024.Although March saw a slight decrease in dwell times, levels remain above operational norms. Conditions are expected to improve as the weather stabilizes and rail capacity ramps back up by mid to late spring.

US Tariffs

As the U.S. pushes ahead with sweeping tariffs, the ripple effects are starting to be felt across APAC. According to Drewry, 198 sailings across key east-west routes were cancelled in March and April alone. That capacity doesn’t just vanish and the impact on space, schedules and rates will flow through the region in the coming weeks/months.

Three key takeaways for Australian businesses:

1. Tariff exposure is no longer predictable

The trade environment (especially for exporters into the U.S.) is shifting rapidly. Between baseline tariffs, China-specific duties, and the potential for semiconductor-focused levies, tariff exposure is now a moving target. That makes cost modelling, pricing strategy, and forecasting far more complex for businesses across the region.

2. Some exporters are pulling out entirely

For certain product categories, the combined tariffs (up to 145%) are so prohibitive that businesses are halting U.S.-bound shipments altogether. That’s not just a short-term pricing issue - it’s a fundamental disruption to long-established trade flows, with potential knock-on effects for production planning, inventory allocation, and market strategy.

3. Country of origin matters more than ever

It doesn’t just matter where your goods are shipped from - it matters where they’re made. This detail is critical. Many Australian businesses may assume they're insulated from tariffs because of FTA status, but if their goods are manufactured in China, they’re still exposed to China-specific duties. The rules around origin and transformation now carry major financial consequences.

👉 Read the full breakdown, including example scenarios and strategic responses in our Dedicated Tariffs Blog.

Europe

Europe

.png)

Ocean freight rates

- Shanghai to Rotterdam: Increased by 4% (up $88) to $2,392 per 40ft container.

- Shanghai to Genoa: Rose by 1% to $3,071 per 40ft container.

- Rotterdam to Shanghai: Up 2% to $475 per 40ft container.

- Rotterdam to New York: Increased by 1% to $2,153 per 40ft container.

- New York to Rotterdam: Decreased by 1% (down $7) to $824 per 40ft container.

These adjustments reflect a tightening of capacity and the early impacts of recent tariff changes. Drewry anticipates further rate increases in the coming weeks due to ongoing capacity reductions and tariff pressures. Drewry

- Rates ex Europe to Australia remain stable with no change to current rate levels.

Capacity and schedule reliability

Capacity

- April has seen a notable reduction in blank sailings compared to March, with the majority affecting East Mediterranean exports. Port congestion continues to impact schedules across key hubs, including Piraeus, Mersin, and Valencia in the Mediterranean, as well as Hamburg, Antwerp, and Rotterdam in Northern Europe.

- Equipment remains tight across several parts of Central Europe, with notable shortages reported in Austria, Slovakia, Switzerland, Hungary, and the southern and eastern regions of Germany.

Schedule reliability

🇩🇪 Germany

Hamburg:

The implementation of limited gate-in windows for export cargo has eased yard congestion across several terminals. Vessel operations are running smoothly, with no major issues reported. Vessel lineups remain full, and labour availability is stable.

River Rhine:

Water levels continue to be low at key points—Kaub, Köln, and Duisburg Ruhrort—restricting barge capacity to and from several terminals. However, feeder services between Antwerp and Rotterdam remain unaffected.

🇧🇪 Belgium

Antwerp – PSA Terminal:

Yards are over capacity for reefers and empty containers and at critical levels for dry containers. Vessel productivity remains below standard, and backlogs from last week’s strike have caused significant delays. To ease yard pressure:

Empty containers are no longer being accepted.

Yard opening times have been reduced from 7 to 5 days.

This situation is expected to persist until late April.

Antwerp – AGW Terminal:

The recent strike also impacted vessel lineups at AGW. However, yard utilisation remains stable.

🇳🇱 Netherlands

Rotterdam – ECT:

Labour and yard utilisation have improved, but delays remain:

Feeders are delayed 48–72 hours

Barges are delayed 24–48 hours

The delivery of new gantry cranes on 4 April is occupying a feeder berth until end-April, adding strain to operations. Phase-in/phase-out vessel activity continues to impact terminal efficiency

🇮🇹 Italy

Labour Action Updates:

Ongoing and upcoming strikes are expected to disrupt rail and port operations:

11 April (24-hour strike): Anticipated to affect Genoa port operations, including gate access and container transport.

5 May, 21:00 – 6 May, 21:00: Rail operations will be suspended during this period.

🇬🇧 United Kingdom

London Gateway:

Average vessel waiting times have risen to approximately 2.4 days.

Yard utilisation is at 78%

Reefer utilisation has dropped to 67%

High volumes of empty containers are present. Crane maintenance (part of a 10-year plan) is ongoing. Increased vessel calls—some without berthing windows—along with reduced transhipment moves and phase-in/out activity continue to challenge operational flow.

Global air freight

- In the week ending April 6, 2025, global air cargo volumes experienced a significant 7% week-on-week decline, as reported by WorldACD. This drop is attributed to the Eid-al-Fitr holiday, which led to reduced shipping activity in several countries, and to growing global trade uncertainties, including the imposition of new U.S. tariffs and the removal of de minimis exemptions for shipments from China and Hong Kong. Source: Asian Aviation

- Despite the decrease in cargo volumes, air freight rates have remained resilient. Worldwide average rates increased by 2% week-on-week, reaching $2.52 per kilogram, marking a 3% rise compared to the same period last year. Notably, spot rates from the Asia Pacific region saw a 5% week-on-week increase, averaging $3.94 per kilogram. Source: Asian Aviation

- Regionally, the most significant declines in cargo volumes were observed in the Middle East & South Asia (-24%) and Africa (-21%), with countries like Pakistan, Egypt, and Bangladesh experiencing drops of up to 50%. These reductions are largely attributed to the Eid holiday. Looking ahead, the air cargo industry faces potential challenges due to escalating trade tensions and shifting tariff policies, which may further impact global trade flows. Source: Asian Aviation

- Strong winds in northern China, particularly Beijing, have caused the cancellation of over 400 flights, infrastructure damage, and the closure of major tourist attractions. The winds, which could break historical records, also led to the postponement of events, including a half-marathon. Source: CNA

- The market into Australia has been fluid in recent weeks, with strong e-commerce demand driving rates up.

- PVG offers open space for week 16, with a slight dip in pricing. BNE space is tight.

- CAN pricing is on the rise, with space tight - particularly into BNE. SYD/MEL can expect standby flights. Space is not readily available until the end of the week.

- PEK has seen a reduction in rates, with space available later in the week to the East Coast airports.

- SZX/HKG has seen a reduction in pricing with space readily available from mid-week to SYD/MEL.

General news

- Panama’s Comptroller General declared the 2021 renewal of CK Hutchison’s port concession illegal, citing lack of proper authorization, potentially costing the country $1.3 billion. The controversy threatens a $22.8 billion deal involving BlackRock’s acquisition of CK Hutchison’s global port assets and has drawn geopolitical attention from the U.S. and China. Source: WorldCargoNews

- Severe Storms and Tornadoes across the Midwest and Southern U.S. over the weekend have killed at least 22 people, with Tennessee reporting the highest toll. Victims include children, elderly, and even a volunteer firefighter.

- Widespread Flooding and Damage: Swollen rivers, fallen trees, and tornado damage forced evacuations in cities like Frankfort, Kentucky. Millions were under flood watch, and key events like the Masters Tournament faced disruptions due to severe weather. Source: BBC

- Tropical Cyclone Errol is forming off the northern coast of Western Australia, with the Bureau of Meteorology (BoM) forecasting its development from a tropical low into a cyclone by Sunday morning. As of Saturday afternoon, the system was approximately 335 km north of Kalumburu, moving west-southwest. Projections indicate it could intensify to a Category 3 cyclone by Tuesday, though it's not expected to make landfall. Source: ABC

- India has revoked a key transshipment facility that allowed Bangladeshi exports to third countries via Indian land borders, citing delays and higher costs affecting its own exports. This decision is expected to disrupt Bangladesh's trade, particularly in ready-made garments, and increase logistical costs, potentially straining regional economic cooperation. Source: Logistics Insider

Interesting Articles

- Shipping giants face surging demand before tariffs hit global freight (AFR)

- ‘Tariff shockwave’ leads to collapse in ocean container bookings

- Pre-tariff rush of goods from US to China sees air rates soar, but not for long

- Disastrous' DSV-Schenker merger would 'disrupt European haulage market'

- De minimis-induced ecommerce demand slump could cripple freighter operators

- North America was the top site for logistics acquisitions in March

- Temporary tariff relief brings on early transpacific peak season

.avif)

Experienced Business Development Manager with a demonstrated history of working in the logistics and supply chain industry. Skilled in Import/Export, Freight Transportation, Freight, Warehouse Operations, and Overseas Networking.

Frequently Asked Questions

Explorate gives supply chain managers one real-time view across ever forwarder, lane and mode without replacing your current process, partners or systems.